Trader Hub

Yoma Strategic Holdings Ltd. – Cost-control Mitigation

traderhub8

Publish date: Wed, 19 May 2021, 11:11 AM

- 1H21 net profit in line, at 54% of our FY21e estimate. Held up by real-estate recognition. Yoma continued to cut costs and capex to conserve cash.

- F&B and Motors hardest hit by Covid-19 and coup d’état. Yoma may close up to one third of its restaurants. Construction of Yoma Central has been suspended.

- Maintain NEUTRAL with lower TP of S$0.147, down from S$0.156. This remains pegged at 0.45x P/BV, slightly above 2007-2010 average P/B during major conflicts, political upheavals and natural disasters. We cut FY21e book value per share by 8% to US$0.244 to reflect the depreciation of MMK/US$.

The Positives

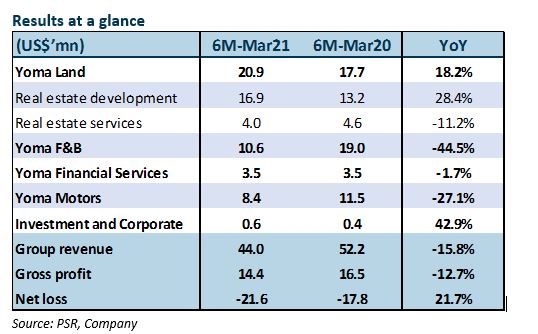

+ Real-estate revenue despite construction delays. 1H21 revenue and net profit met, at 54% of our FY21e forecasts. Topline was propped up by real-estate recognition. Construction of Star Villas, a new project in Star City, commenced in December 2020. Development revenue increased 28.4% YoY from sales of a penthouse at The Peninsula Residences, Star Villas units and new projects at Pun Hlaing Estate as construction progressed. Lower revenue from City Loft was recognised due to construction delays.

+ Slashed costs. Yoma cut operating costs and deferred the bulk of its capex to conserve cash. Staff costs were slashed by more than 60% through job cuts, furloughs and pay reductions. The company also reduced inventory and monetised existing PPE stock. As such, administrative expenses declined 19.5% YoY. Interest expenses dropped 14.2% from lower interest rates. As more stringent financial management has been implemented since 1 February 2021, cost-efficiency gains should be realised in the coming months. We lower FY21/FY22e administrative expenses by 15%/20%.

The Negatives

– F&B hardest hit by Covid-19 and coup d’état. The restaurant business, which was already reeling under Covid-19, has been dealt further blows by the coup since 1 February 2021. Temporary store closures were frequent and operating hours shortened against a backdrop of weaker consumer sentiment. Operational disruptions to delivery aggregators due to trade-zone topsy-turvy, safety measures and a suspension of food-delivery apps reduced delivery channel sales. Delivery sales constituted 50% of F&B revenue during Covid-19. As a result, 1H21 F&B revenue fell 44.5% YoY.

– Motors second to F&B. Heavy equipment was equally affected by disruptions to hire-purchase financing from local banks and delays in port clearances. Despite strong sales of Ducati motorbikes, the automotive business was hit by the closure of vehicle registration offices and dealer showrooms. Consequently, 1H21 motor revenue slipped 27.1% YoY.

Source: Phillip Capital Research - 19 May 2021

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

Johor house best buy

2

CEO Morning Brief

Singapore Post Shares Slide After CEO Fired Over Whistleblower Report

3

4

CEO Morning Brief

DBS Shares’ 43% Rally Seen Having More Legs as Wealth Fees Rise

5

CEO Morning Brief

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....