Trader Hub

NetLink NBN – Trust Stable as Expected

traderhub8

Publish date: Mon, 17 May 2021, 09:26 AM

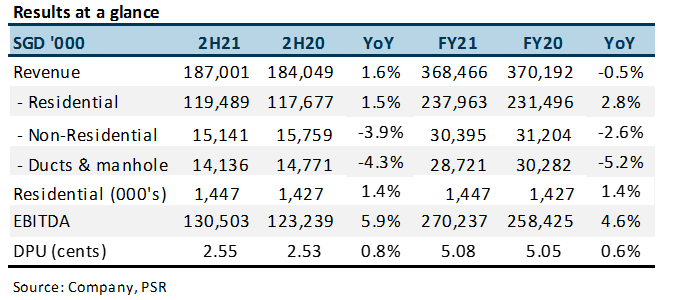

- Revenue and EBITDA in FY21 modestly below expectations, at 98%/95% of our FY21e forecasts due to write-off of IT assets.

- FY21 DPU up 0.6% YoY to 5.08 cents (FY20: 5.05 cents). Current annual distribution of S$198mn backed by operating cash flows of S$264mn.

- Core residential revenue expanded 1.5% YoY in 2H21, in tandem with a 1.4% improvement in fibre connections to 1.44mn. Net adds slowed down to 9,424 residentials in 2H21 (1H21 9,915; 2H20 16,818).

- ACCUMULATE rating and DCF TP of S$1.03 (WACC 5.9%) unchanged. Dividend yield of 5.2% supported by monthly recurring revenue from 1.44m residential fibre connections. Growth to be sustained by estimated 25,000 new residential homes per year. Company is exploring telecommunication infrastructure opportunities overseas, including emerging countries and minority stakes.

The Positive

+ Core residential revenue stable. Core residential revenue was up 1.5% YoY in 2H21 to S$119.4mn as it added 9,424 residential connections. The impact of the pandemic was indirect, from a slower build-out of homes in the country. Our forecast for FY22e connections is 25,000 net additions (FY21: 19,339).

The Negative

– Non-residential and ducts & manholes the weaker spots. Non-residential revenue contracted 4% YoY despite a modest 0.9% YoY improvement in connections to 48,108. Competition had resulted in rebates for customers. Ducts are expected to decline further with a drop in customer projects.

Outlook

We expect another stable year in FY22e. Capex should be higher as reflected by a S$12.4mn rise in capital commitments to S$48.7mn. NBAP revenue is likely to gain traction from 5G rollout, although contributions remain marginal at 3% of revenue.

Maintain ACCUMULATE and TP of S$1.03

NetLink generates stable 5.2% distribution yields. Lockdowns will only result in delays in installations, diversions and co-location revenue, which account for a combined 13% of revenue.

Source: Phillip Capital Research - 17 May 2021

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Trade Confidently & Analyze Charts Conveniently - Download VCPlus IOS & Android App Now!

Latest Videos

Apps

Top Articles

1

Johor house best buy

2

CEO Morning Brief

Singapore Post Shares Slide After CEO Fired Over Whistleblower Report

3

4

CEO Morning Brief

DBS Shares’ 43% Rally Seen Having More Legs as Wealth Fees Rise

5

CEO Morning Brief

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....