Trader Hub

Asian Pay Television Trust-Free Cash Flows Stable

traderhub8

Publish date: Fri, 14 May 2021, 09:27 AM

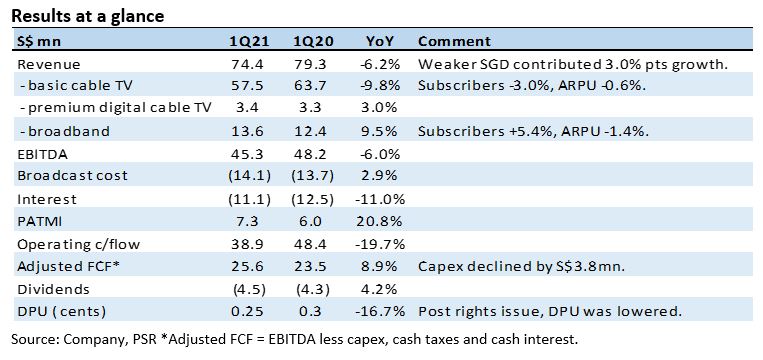

- 1Q21 revenue and EBITDA were within expectations, at 26%/25% of our FY21e forecasts.

- Revenue was down S$5mn or 6% YoY, dragged down by a 9.8% contraction in cable TV. Weakness was partly offset by a 9.5% rise in broadband revenue. FCFs rose modestly to S$25mn from a S$4mn decline in capex.

- DPU guidance of 0.25 cent/quarter for FY21e maintained. BUY recommendation and target price of S$0.15 unchanged. Stock pegged at 9x FY21e EV/EBITDA, a 20% discount to Taiwanese peers for its smaller scale, higher leverage and weaker growth profile. Annual dividend distribution of S$18mn well supported by FCF of S$77mn. 5G data backhaul to be key component of broadband business in the next few years, though we have yet to model any revenue.

The Positive

+ Growth in broadband. Broadband revenue expanded almost 10% YoY in 1Q21. Net subscriber adds were 5,000, the highest in four quarters with ARPU almost unchanged. APTT has been partnering wireless operator shops to distribute their high-end 500MB/1GB broadband plans since end-2019.

The Negative

– Cable TV still shrinking. Cable TV revenue declined around 10% YoY in 1Q21. Subscription revenue was stable at S$49mn but non-subscription dropped 43% to S$8.4mn due to an absence of in-house content sales and lower channel leasing revenue. Both were popular during the lockdown in Taiwan.

Outlook

We expect FCF to be stable despite weaker revenue as capex is trending down the next two years. Investments in the past three years have driven homes to fibre node density from 750 to 250 currently. This should be sufficient to meet demand for 5G data backhaul. We lower our FY21e capex by 10% to S$45mn.

Maintain BUY and target price of S$0.15

Current dividend yield of 9% from a S$18mn payout is well supported by FCF of S$77mn. Our FY21e earnings forecast is largely unchanged.

Source: Phillip Capital Research - 14 May 2021

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

Johor house best buy

2

CEO Morning Brief

Singapore Post Shares Slide After CEO Fired Over Whistleblower Report

3

4

CEO Morning Brief

DBS Shares’ 43% Rally Seen Having More Legs as Wealth Fees Rise

5

CEO Morning Brief

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....