Trader Hub

Fortress Minerals Ltd Continued Outperformance

traderhub8

Publish date: Mon, 26 Apr 2021, 09:48 AM

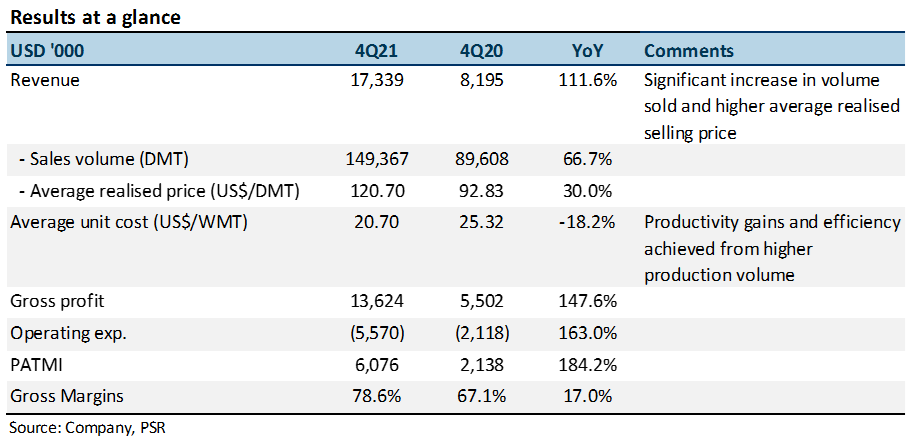

- 4QFY21 results beat, with FY21 revenue and PATMI at 122%/116% of our forecasts. Volume sales growth of 66.7% YoY in 4QFY21 exceeded our +12.8%. Gross margin of 78.6% and ASP of US$120.70/DMT also beat our forecasts of 74.3% and US$96.00/DMT.

- 4QFY21 PATMI tripled YoY to US$6mn from higher selling prices and an 18% decline in unit production costs.

- Maintain BUY with higher TP of S$0.64 from S$0.47 as we roll over our 11x P/E target to FY22e, still in line with industry average. Our FY22e PATMI has been raised by 27% to US$21.8mn as we increase our production forecast by 12% to 498,032 DMT. Iron ore prices are expected to remain elevated with a rebound in steel production and supply disruptions.

The Positives

+ Steady increase in volume. Iron ore concentrates sold increased 66.7% YoY by volume in 4QFY21 and 67.9% in FY21. This lifted revenue by 111.6% in 4QFY21 and 84.1% in FY21. QoQ, volume sold and revenue were higher by 60.2% and 68.3% respectively.

+ Spike in margins. Gross profits more than doubled from US$5.5mn in 4QFY20 to US$13.6mn in 4QFY21. Gross profit margins rose from 67.1% to 78.6%. This was achieved with higher realised ASPs of iron ore concentrates, which went from US$92.83/DMT in 4QFY20 to US$120.70/DMT in 4QFY21. Unit costs also decreased from US$25.32/WMT to US$20.70/WMT with the help of efficiency gains.

+ Operating cash flow turned positive. Operating cash flow turned from a negative US$11k in 4QFY20 to a positive US$2.7mn in 4QFY21. 4QFY21 FCF remained a negative US$4.2mn vs. -US$478k in 4QFY20 from a spike in capex. Full year, FCF increased to US$7.1mn from US$4.8mn in FY20.

The Negative

– Spike in capex. Capex jumped from US$390k in 4QFY20 to US$3.6mn in 4QFY21, as FML expanded its truck fleet and reinvested in its Bukit Besi mine for further exploration works.

Source: Phillip Capital Research - 26 Apr 2021

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Trade Confidently & Analyze Charts Conveniently - Download VCPlus IOS & Android App Now!

Latest Videos

Apps

Top Articles

1

Johor house best buy

2

CEO Morning Brief

Singapore Post Shares Slide After CEO Fired Over Whistleblower Report

3

4

CEO Morning Brief

DBS Shares’ 43% Rally Seen Having More Legs as Wealth Fees Rise

5

CEO Morning Brief

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....