Trader Hub

Singapore Banking Monthly Extending Their Green Shoots

traderhub8

Publish date: Mon, 05 Apr 2021, 09:18 AM

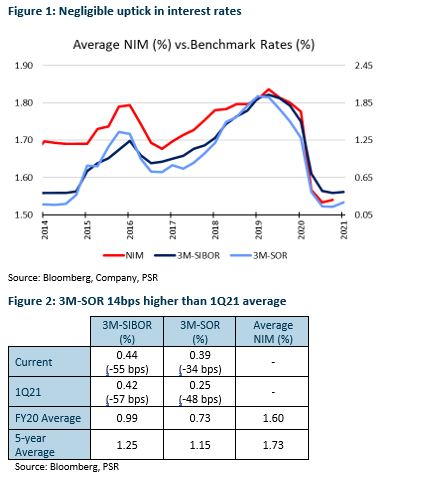

- Current interest rates of 0.42% are 11bps higher than the start of the year.

- Loans fell 0.88% YoY in February but grew 0.46% MoM, the fourth consecutive month of growth.

- SGX’s SDAV was third-highest on record but down YoY alongside DDAV as there was an anomalous selloff during the COVID-19 outbreak last year.

- Maintain Overweight. Loans remain on path for recovery and interest rates are stable with a positive economic outlook. We continue to prefer OCBC (OCBC SP, BUY, TP: S$13.65) for its WM and insurance franchises.

Interest rates ticked up in March

Interest rates edged higher for a second consecutive month to 0.42% in March. Year to March, they were up 11bps. Still, the rates were 53bps lower than their FY20 average. We continue to expect FY21e NIMs to come in at 1.45-1.55% for the three banks, lower than their 1.60% average in FY20.

Investment action

Maintain Overweight

Despite the run-up in their share prices in 1Q21, we continue to see upside for banks. They had traded above 1.4x P/B before in the past five years and are currently trading close to or below our P/B targets of 1.17-1.31x (Figure 10). Our targets are supported by improving ROEs as allowances ease off in FY21e.

The banks have also emerged from FY20 with stronger capital ratios of 13.9-15.2%. These are higher than their ideal operating range of 12.5-13.5%, which banks hope to achieve so as to not negatively impact ROEs from holding excess capital. This should support a resumption of pre-COVID dividend payouts once the MAS lifts restrictions.

For sector exposure, we continue to prefer OCBC. OCBC is expected to book faster earnings growth from its wealth-management and insurance franchises as market conditions improve.

Source: Phillip Capital Research - 5 Apr 2021

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Trade Confidently & Analyze Charts Conveniently - Download VCPlus IOS & Android App Now!

Latest Videos

Apps

Top Articles

1

Johor house best buy

2

CEO Morning Brief

Singapore Post Shares Slide After CEO Fired Over Whistleblower Report

3

4

CEO Morning Brief

DBS Shares’ 43% Rally Seen Having More Legs as Wealth Fees Rise

5

CEO Morning Brief

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....