Trader Hub

United Overseas Bank Limited - Sun Is Coming Out Again

traderhub8

Publish date: Tue, 02 Mar 2021, 09:24 AM

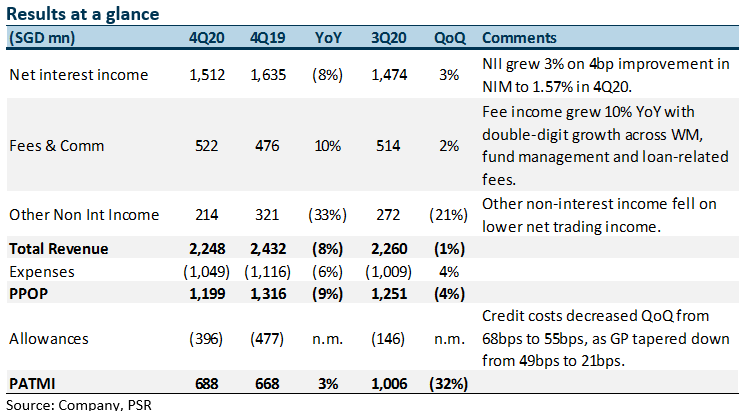

- FY20 earnings of S$2.94bn met, at 2% of our estimate.

- NIM recovered QoQ to 1.57% to boost NII by 3%.

- Fees and commissions grew QoQ and YoY, though trading income was lower.

- Commitment to 50% payouts implies FY21e DPS of S$1.20 on strong CET-1 of 14.7%.

- Upgrade to ACCUMULATE from NEUTRAL with higher GGM TP of S$28.70 from S$21.10. We raise FY21e earnings by 22% to reflect double-digit growth in fees and commissions as well as tapered credit costs. We continue to peg TP at 1.17x P/BV but lower COE from 8.9% to 8.5% on lower risks. We also forecast a higher 6% ROE from better profitability.

The Positives

+ Resilient interest margins

NIM improved 4bps QoQ from 1.53% to 1.57%, contributing to a 3% increase in NII. Better management of liquidity and funding costs lifted NIM. NIM is expected to be stable as the bank targets loan growth to improve NII. Room for further funding-costs adjustments and improving LDR can help manage NIM compression pressures.

+ Robust growth in fees and commissions

Fee and commission income grew 10% YoY and 2% QoQ. Fund-management and wealth-management fees improved, particularly as UOB’s wealth-management franchise gained traction. Credit-card fees also grew by double digits for a second consecutive quarter to S$109mn, mirroring a recovery in consumer spending.

The Negatives

– Weak trading income

Volatile market conditions caused its trading income to decline. This reduced its non-interest income by 33% YoY and 21% QoQ. The QoQ decline was also due to more investment gains booked during the previous quarter. As volatility subsides, we expect trading income to stabilise in FY21e.

Source: Phillip Capital Research - 2 Mar 2021

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Trade Confidently & Analyze Charts Conveniently - Download VCPlus IOS & Android App Now!

Latest Videos

Apps

Top Articles

1

Johor house best buy

2

CEO Morning Brief

Singapore Post Shares Slide After CEO Fired Over Whistleblower Report

3

4

CEO Morning Brief

DBS Shares’ 43% Rally Seen Having More Legs as Wealth Fees Rise

5

CEO Morning Brief

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....