Trader Hub

IREIT GLOBAL Another Year of Resilience

traderhub8

Publish date: Mon, 01 Mar 2021, 09:25 AM

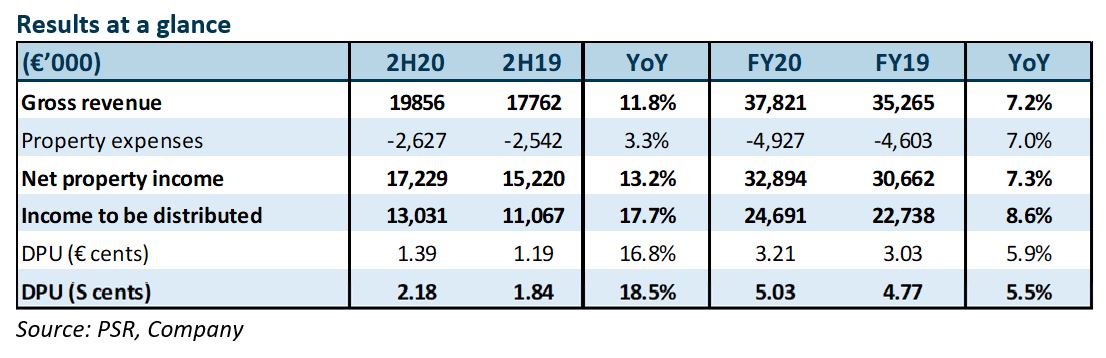

- FY20 NPI and DPU at 102%/103% of our forecasts, in line. Rental collection exceeded 99%.

- FY21 lease breaks/expiries minimal at 3.7%/3.3%. Portfolio occupancy remained high at 95.8%. Portfolio valuation increased by 1.2% with high occupancies anchored by blue-chip tenants in German portfolio.

- Maintain ACCUMULATE with raised DDM TP (7.85% discount rate) of S$0.70, from S$0.68. Our TP implies yields of 7.3% and total prospective returns of 14.2%. FY21e DPU has been raised by 7% for better operational performance.

The Positives

+ FY20 better than expected, rental collection high. Gross revenue and NPI in FY20 were up 7.2% and 7.3% YoY respectively, following consolidation of its Spanish properties after their acquisition on 22 October 2020. FY20 NPI, distributable income and DPU were slightly better than expected, at 102%/104%/103% of forecasts. Rental collection exceeded 99%. Outstanding were rental rebates and deferrals granted to a few tenants.

+ High portfolio occupancy, minimal FY21 expiries, stable portfolio valuation. Portfolio occupancy remained high at 95.8%, though down 0.5% from a quarter ago as two tenants exercised their break option at Delta Nova IV. FY21 lease breaks/expiries are minimal at 3.7%/3.3% by gross rental income (GRI). Despite Covid-19, portfolio valuation increased by 1.2%. High occupancy of 99.6% anchored by blue-chip tenants led to a 2.3% valuation increase for its German portfolio. This constituted 82% of its total portfolio valuation. Valuation of its Spanish portfolio, in contrast, was down 3.5% due to longer vacancy assumptions.

The Negative

– Chunky FY22 expiries, 5% likely de-risked. About 32.5%/24.6% of leases by GRI will be due for lease breaks/expiries in FY22. About 5% of the lease breaks are attributable to DRB* for its lease at Berlin Campus due in June 2022. DRB is likely to keep its lease as rental rates are attractive. It recently leased a new building adjacent to Berlin Campus for more than double Berlin Campus’ passing rents. Other properties up for lease breaks/expiries are IREIT’s Darmstadt and Munster Campus, leased by Deutsche Telekom (DT). IREIT has started to engage DT for early renewals.

*DRB – Deutsche Rentenversicherung Bund

Outlook

With lockdown extensions and strict social-distancing restrictions in several economies, a sustainable recovery in the European real estate remains largely uncertain. Though work-from-home is taking roots, it remains too early to predict the direction of office demand as work arrangements are still in a flux. To date, physical occupancies in its portfolio amount to 30%.

After its rights issue in 4Q20, aggregate leverage improved to 34.8% in FY20 from 39.3% a year ago. Weighted average debt to maturity was 5.3 years, with all borrowings due to mature only in 2026. This provides IREIT with the flexibility to pursue M&A growth opportunities. It is looking at office, retail and logistics assets in Europe, particularly in countries where Tikehau Capital has a foothold such as France, Italy and the Netherlands.

To provide more options to its unitholders, IREIT is exploring the possibility of implementing dual-currency (€/S$) trading. Although its S$ trading liquidity may be compromised, we believe dual-currency trading will help to attract European investors looking for exposure to a pure Western Europe office portfolio. IREIT is also considering changing its distribution currency from S$ to its functional currency, €. If implemented, it will not need to hedge future distributions. This is more efficient, in our view, as IREIT can focus purely on operational metrics.

Maintain ACCUMULATE with raised TP of S$0.70. FY21e DPU has been raised by 7% for better operational performances. Current price implies dividend yields of 7.3% and total prospective returns of 14.2%.

Source: Phillip Capital Research - 1 Mar 2021

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Trade Confidently & Analyze Charts Conveniently - Download VCPlus IOS & Android App Now!

Latest Videos

Apps

Top Articles

1

RHB Investment Research Reports

2

CEO Morning Brief

Keppel DC REIT Buys Data Centres in Singapore’s Genting Lane for S$1b

3

4

CEO Morning Brief

Marina Bay Sands Eyes Singapore’s Largest Loan of US$9b — Bloomberg

5

CEO Morning Brief

WeWork Gives Up Singapore Locations in Sign of Co-working Woes

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....