Trader Hub

Keppel DC REIT – Riding Technology Growth

traderhub8

Publish date: Mon, 01 Feb 2021, 07:28 PM

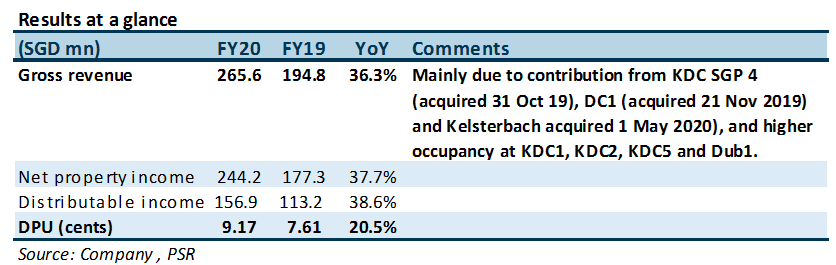

- FY20 DPU of 9.17 Scts (+20.5% YoY) was in line, forming 97.1% of our estimate.

- Earnings improved on the back of acquisitions and higher portfolio occupancy.

- Upgrade to ACCUMULATE from NEUTRAL with DDM-based TP raised from S$2.91 to S$3.20 (COE 5.75%) after we raise occupancy. We assume S$500mn of acquisitions in our forecasts.

+ Positives

+ FY20 NPI and DPU grew 37.7% and 20.5% YoY respectively, led by newly-acquired KDC4 and DC1 in Singapore (in 2H19) and Kelsterbach DC in Germany (on 1 May 2020). Portfolio occupancy was also higher from completed AEI and higher demand.

+ Portfolio occupancy improved QoQ from 96.7% to 97.8% (FY19: 94.9%). Higher occupancy in 4Q20 stemmed from: 1) the handover of newly converted DC space at KDC5 which lifted occupancy from 84.2% to 100%; 2) tenant expansion at KDC1 which increased occupancy from 89.2% to 91.1%; and 3) a new tenant at KDC2 which raised occupancy from 93.5% to 98.2%. AEI to bring more power onsite at Dub1 also allowed KDC to lease out additional space, bumping up its occupancy from 61.8% to 81.1%.

+ Acquired Amsterdam DC on 24 Dec 2020 for S$48.1mn; initial NPI yield of 5.1%. Amsterdam DC comprises a shell & core data centre and an office component, with occupancy of 99.1%. The asset is located near the Amsterdam Internet Exchange, one of the world’s largest hubs in terms of connections and traffic. Amsterdam DC has an occupancy of 99.1% and is leased to data-centre and IT service firms.

– Negative

– Natural decay of leases reduced WALE to 6.8 years (FY19: 8.6 years). Colocation (Colo) leases are the most profitable leases as rents include charges for facility management and the rental of M&E equipment. However, Colo leases typically run on shorter WALEs of 2.7 years vs. 11.2 years for fully-fitted and 7.3 years for shell & core data centres. Fortuitously, most of KDC’s Colo leases are in Singapore, which is a rising rental market due to limited new supply. As such, shorter WALEs should allow KDC to capture higher rents as the leases are marked to market upon renewal. In contrast, with a WALE of 1.5% and persistently low occupancy of 63.1%, KDC’s struggling Malaysian asset, Basis Bay (0.8% of AUM), may face occupancy risks should its existing tenant decide not to renew.

Outlook

Evaluating potential acquisitions. KDC is evaluating several piecemeal and portfolio acquisitions with cap rates of 5-7%. However, travel restrictions in several countries have prevented KDC from physically inspecting the assets overseas. Management has found a way around this, which is to focus on shell & core assets which are more passive in nature and rely on third-party valuers. Using this strategy, KDC was able to acquire Amsterdam DC before the year ended.

Demand-supply gap to push up market rents. Singapore is KDC’s core market, accounting for 56% of its AUM. Given the moratorium on data centres in Singapore, we expect market rents to be bid up in the coming two years. Present higher demand has led to higher occupancy for KDC’s portfolio, though market rents have not moved. While KDC’s portfolio occupancy in Singapore is high at 97.0%, Colo leases in Singapore have WALEs of 1.4-4.0 years. These coincide with expected rent appreciation. In the meantime, KDC is expected to benefit from organic growth as many of its leases have built-in periodic rental escalations averaging 2-4% p.a.

Upgrade to ACCUMULATE, DDM-based TP raised from S$2.91 to S$3.20

Changes from our previous report

Our DDM-based TP has been raised to reflect higher occupancy and asset productivity following AEI, which raises our NPI by 6.9% on a same store basis (excluding any acquisition assumption). Our previous TP of S$2.91 assumes that KDC will make a S$500mn of acquisitions in 1Q21e (NPI yield 6% and LTV 30%). In this report, we push back our S$500mn acquisition assumption (NPI yield 6% and LTV 30%) from 1Q21 to 4Q21.

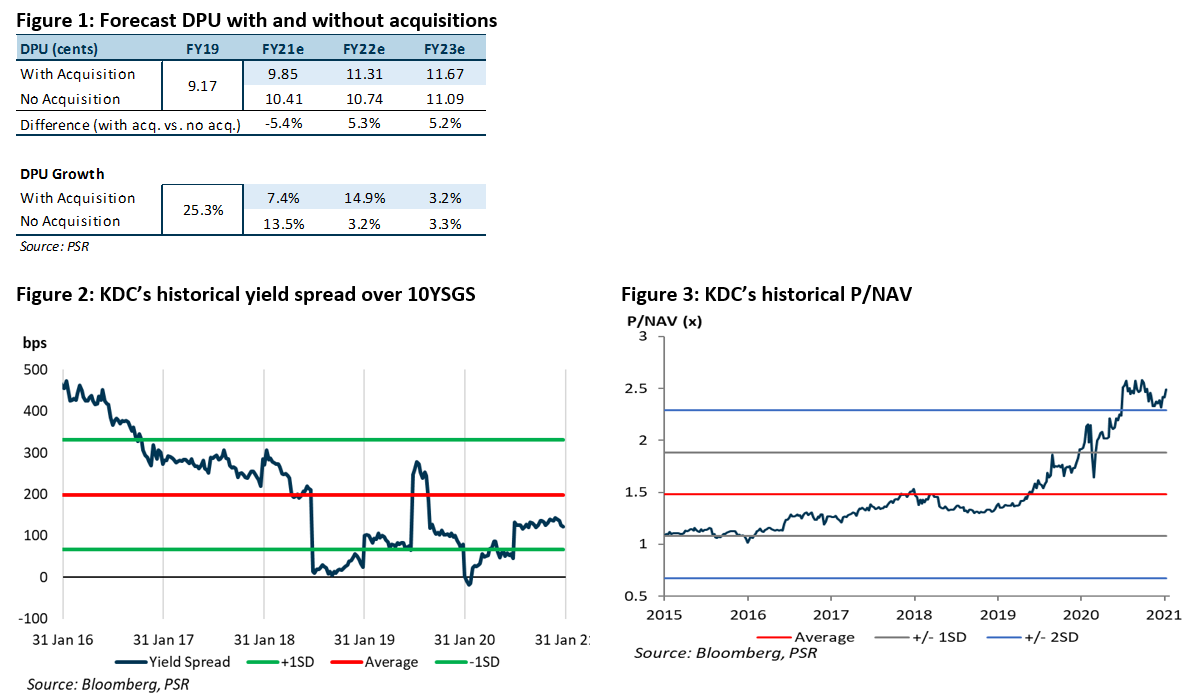

Scenario analysis: with and without acquisitions

Our acquisition assumption reduces FY21e DPU by 5.4% due to an enlarged share base, but increases FY22e DPU by 5.3% (Figure 1).

Demand for data centres is supported by increasing 5G, smartphone and cloud adoption. KDC’s higher P/NAV of 2.4x (Figure 3) is supported by the forecast growth in data centres and its ability to deliver earnings growth through AEI, rental improvements and accretive acquisitions. We forecast DPU yields of 3.3%/3.8% for FY20e/21e, which should deliver a forward yield spread of 220bps, the average of its five-year historical yield spread over 10YSGS (Figure 2).

Source: Phillip Capital Research - 1 Feb 2021

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

Johor house best buy

2

CEO Morning Brief

Singapore Post Shares Slide After CEO Fired Over Whistleblower Report

3

4

CEO Morning Brief

DBS Shares’ 43% Rally Seen Having More Legs as Wealth Fees Rise

5

CEO Morning Brief

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....