Trader Hub

StarHub Limited – Border Closure Still Hurts

traderhub8

Publish date: Mon, 09 Nov 2020, 09:58 AM

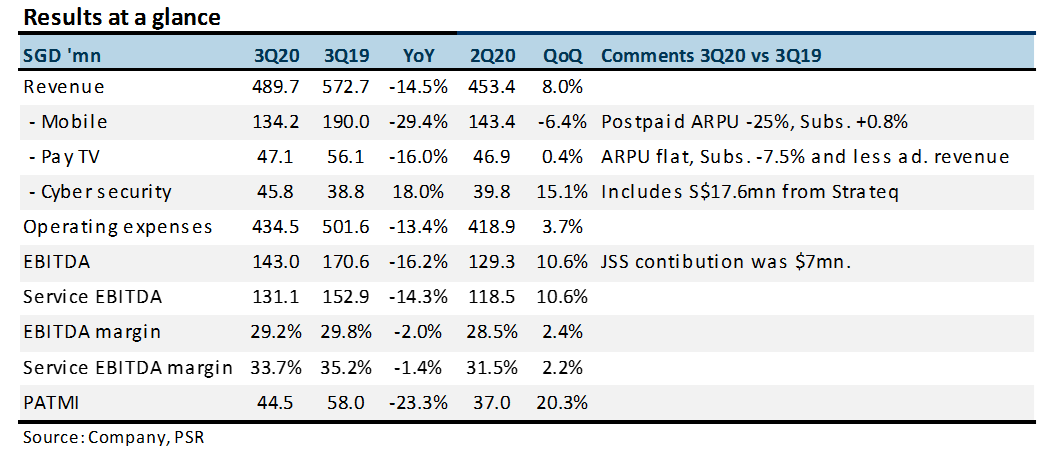

- 3Q20 EBITDA was within expectations, excluding government grants. YTD20 EBITDA was 76% of our FY20e forecast.

- Mobile revenue was down a hefty 29% YoY. This was due to a 25% fall in postpaid ARPU to S$29, a record low. Prepaid subscribers shrank 33% YoY.

- Border closure and loss of roaming revenue to continue to depress earnings. We do see some bright spots. ARPUs for broadband and Pay TV climbed QoQ as promotions ended.

- Maintain NEUTRAL and TP of S$1.24. TP is set at historical 6x EV/EBITDA excluding other income. We raise FY20e EBITDA by 5% to account for another S$15mn in grants in 2H20 and stronger PayTV and broadband businesses. A significant resumption of international travel is key to its earnings recovery. There are little signs yet.

Positive

+ Better QoQ ARPUs for PayTV and broadband. ARPUs for PayTV and broadband rose 2.5% and 7.1% respectively QoQ. Reduced discounts and promotions helped. Revenue for both expanded QoQ due to their better ARPUs.

Negative

– Mobile its Achilles heel. Without roaming revenue, mobile ARPU dived to a record low. Postpaid ARPU was down 25% YoY. Prepaid subscribers shrank by 108k or 33% YoY. There was less demand with fewer tourist arrivals.

Outlook

We lower revenue by 5%. Our forecast for equipment sales was too bullish. We also incorporate revenue from its new acquisition, Strateq. Our EBITDA is raised by 5% to include government grants and an expected uptick in its broadband and PayTV businesses. Enterprise division should enjoy a gradual recovery as projects resume and economic conditions recover. Separately, the launch of non-standalone 5G has garnered a better-than-expected response. Customers are transitioning faster to 5G phones. Faster speeds, lower latency and bundled content subscription have encouraged take-up by niche customers such as gamers and other heavy-content users.

Maintain NEUTRAL and TP of S$1.24

Our valuation is based on 6x FY20e EV/EBITDA. We exclude other income in our EV/EBITDA valuation as it is non-recurring.

Source: Phillip Capital Research - 9 Nov 2020

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

CEO Morning Brief

Keppel DC REIT Buys Data Centres in Singapore’s Genting Lane for S$1b

2

3

CEO Morning Brief

Marina Bay Sands Eyes Singapore’s Largest Loan of US$9b — Bloomberg

4

CEO Morning Brief

WeWork Gives Up Singapore Locations in Sign of Co-working Woes

5

RHB Investment Research Reports

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....