Trader Hub

SATS Ltd – Operations Bottomed But Recovery Subdued

traderhub8

Publish date: Tue, 25 Aug 2020, 10:35 AM

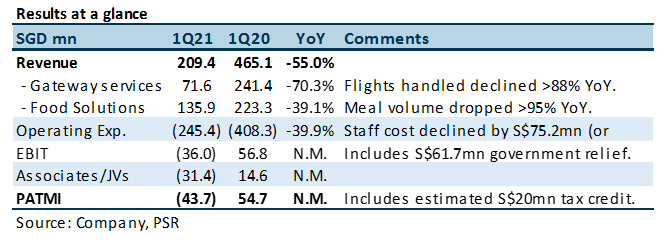

- 1Q21 results were within expectations. Revenue declined 55% YoY to S$209mn with a net loss of S$43mn in 1Q21.

- The net loss was after tax credit and government relief of totalling around S$80mn.

- Operationally the airport traffic has bottomed but any recovery will be tepid. We maintain our SELL recommendation with an unchanged target price of S$1.95. Our valuations are pegged to P/B average of 1.35x during the global financial crisis in 2009. The trajectory for any meaningful recovery in air traffic is uncertain and prolonged.

The Positives

+ Restructuring staff cost. Staff cost excluding the S$61.7mn government relief was cut by around 32% YoY in 1Q21. The number of employees has been lowered by 19% YoY to 13,500.

+ Cargo is relatively stronger. Cargo segment has performed relatively better than other segments. Cargo handled declined 51% to 221k in 1Q21, in comparison passengers handled tumbled 99% to 0.2mn.

The Negatives

– Associates a major source of weakness. With government relief, SATS suffered an operating loss of S$36mn. It was comparable to the S$31mn losses by associates and joint venture. China was the largest drag to associates. The closure of Beijing Daxing Airport was a reason for the losses in China.

Outlook

FCF in 1Q21 was a negative $71mn. With a cash balance of S$723mn (net debt: S$152mn), SATS can easily ride out the current downturn or another 10 quarters of the similar level of FCF cash burn-rate. SATS has likely bottomed out operationally but we worry such listless conditions may persist for another three to four quarters.

Maintain SELL with a target price of S$1.95

Without any clarity of a sustainable and material improvement in air travel and net losses to persist for the company, we maintain our SELL recommendation with an unchanged target price of S$1.95. Our forecast is unchanged.

Source: Phillip Capital Research - 25 Aug 2020

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Trade Confidently & Analyze Charts Conveniently - Download VCPlus IOS & Android App Now!

Latest Videos

Apps

Top Articles

1

CEO Morning Brief

2

CEO Morning Brief

Singapore Post Shares Slide After CEO Fired Over Whistleblower Report

3

4

CEO Morning Brief

DBS Shares’ 43% Rally Seen Having More Legs as Wealth Fees Rise

5

Johor house best buy

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....