Trader Hub

Penguin International Ltd – Cash to Ride This Cycle

traderhub8

Publish date: Wed, 03 Jun 2020, 09:46 AM

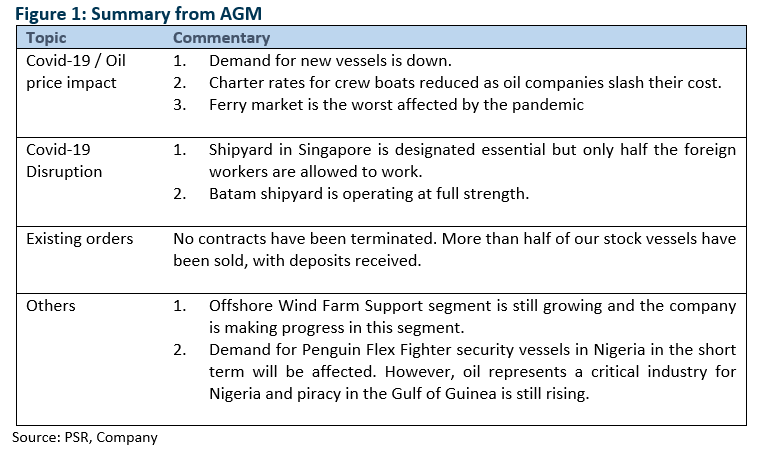

- Penguin provided some business updates in their recent AGM. The outlook is challenging due to Covid-19 and collapse in oil prices.

- Charter rate for crew boats will be under pressure, demand for new vessels is down and ferry customers will suffer from the pandemic.

- We downgrade to ACCUMULATE from BUY. Our FY20e earnings is cut by 52%. The target price is dropped to S$0.55 (prev. S$0.88). We change our methodology from 5x PE (excluding cash) to a P/BV of 0.7x FY20e (historical 10-year average). The net cash of S$60mn (end-Dec19) will allow the company to ride through this turbulence. Net cash is now 52% of market capitalisation.

Downgrade to ACCUMULATE with a lower target price of S$0.55 (prev. S$0.88).

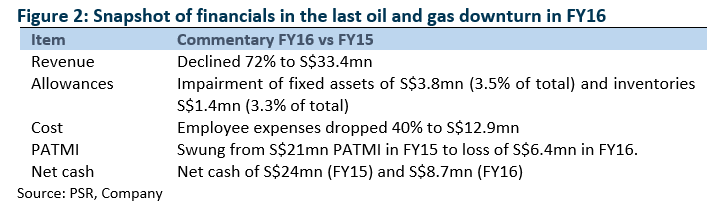

The biggest worry will be trade receivables and inventory of vessels built to stock. During such a stressed environment, the risk will be elevated from customers defaulting payments and inventory becoming unsold. In 2016 downturn, Penguin swung into losses and revenues plunged by 72% (Figure 2). The difference in this cycle is the larger net cash on the balance sheet (from S$24mn end 2015 to S$60mn end 2019) and a more diverse portfolio of vessels built.

With such an uncertain earnings outlook, we will use price to book as a gauge to valuations.

The 10-year price to book average is 0.7x, with a range of 0.5x to 1x. Penguin can ride out the downtrend in the industry with their large cash hoard.

Source: Phillip Capital Research - 3 Jun 2020

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

CEO Morning Brief

2

CEO Morning Brief

DBS Shares’ 43% Rally Seen Having More Legs as Wealth Fees Rise

3

CEO Morning Brief

Singapore Post Shares Slide After CEO Fired Over Whistleblower Report

4

5

Johor house best buy

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....