Trader Hub

Thai Beverage PLC – Dry Spell in Watering Hole

traderhub8

Publish date: Mon, 18 May 2020, 10:25 AM

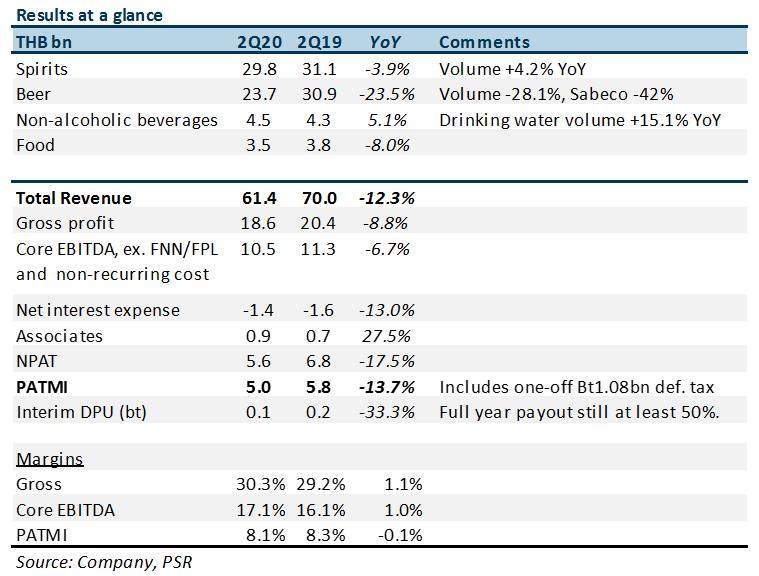

- 2Q20 revenue and earnings were below expectations. The 42% YoY collapse in Sabeco volumes hurt revenue and earnings. Excluding a one-off deferred tax hit of TBH1.08bn, PATMI would have risen 5% YoY.

- Spirits division revenue in 2Q20 declined 3.9% YoY due to weaker volumes but PATMI rose 9.5% YoY due to lower marketing cost.

- The ban in alcohol sales in Thailand from 10 April to 3 May, will temporarily suppress earnings in 3Q20.

- We are lowering our target price to S$0.80 (prev. S$0.95) as we cut earnings by 10%. Our BUY recommendation is unchanged. The slump in volume for Sabeco was worse than expected. And the damage from regulatory changes will linger longer than the current containment measures due to the outbreak. Nevertheless, the spirits business account for close to 90% of group earnings and we expect demand to be more resilient.

The Positives

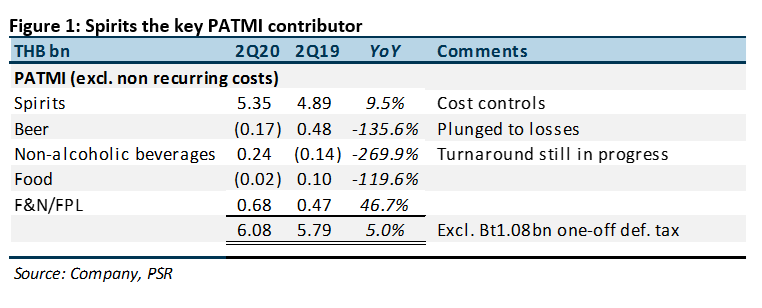

+ Margin stable for spirits business despite weaker volumes. Operating profit for spirits business was flat YoY at TBH6.46bn despite the fall in revenue. The expansion in margins was due to a 10% YoY decline in distribution expenses to TBH1.69bn. Spirits PATMI was up 9.5% YoY to TBH5.35bn and now accounts for 88% of group earnings (Figure 1).

The Negatives

– Sabeco will remain problematic for a few quarters. Sabeco volumes have been punished by three key events: fake new, decree 100 and Covid-19 economic hit. Decree 100 in Vietnam introduced stiffer penalties for drunk driving, ban advertising of alcoholic beverages (between 6pm to 9pm). This has hit the on-trade (aka on-premises) (i.e. pubs, clubs) consumption of beer more than expected.

Outlook

FY20e will be a weaker year for THBEV. Softer economic condition and a collapse in on-trade consumption of alcohol will be the two largest negative impact on revenues. The only positive offset on earnings margins will be lower advertising and promotion activities.

The spirit business in Thailand will remain resilient despite the temporary ban enacted in April. Off-trade consumption (i.e. consumed at home) of spirits contributes approximately 80% of spirit sales and less impacted by Covid-19 social distancing measures. Demand is more linked to farm income levels and overall health of the economy.

More problematic for THBEV will be Sabeco. The stiff penalties for drunk driving in Vietnam will hurt the business more permanently. Some on-trade volumes will be converted to off-trade but there may be some volume slippage is expected. Off-trade margins will be lower as on-trade bottle can be recyclable, thereby reducing cost. Although off-trade volume through modern retail can be higher, the higher percentage of off-trade sales will results in weaker margins.

Maintain BUY with PE-derived TP of S$0.82

We maintain our BUY recommendation. We favour THBEV for their dominant market share of around 90% in spirits. THBEV has an unassailable distribution network in Thailand with 280k direct point of sales presence and another 150k covered indirectly via agents. Another near-term lever to earning in FY20e will be a cut in advertisement and promotion expenses to defend profitability.

Source: Phillip Capital Research - 18 May 2020

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

CEO Morning Brief

2

CEO Morning Brief

DBS Shares’ 43% Rally Seen Having More Legs as Wealth Fees Rise

3

CEO Morning Brief

Singapore Post Shares Slide After CEO Fired Over Whistleblower Report

4

5

Johor house best buy

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....