Trader Hub

Singapore Exchange Limited – Thriving on Volatility

traderhub8

Publish date: Mon, 27 Apr 2020, 04:10 PM

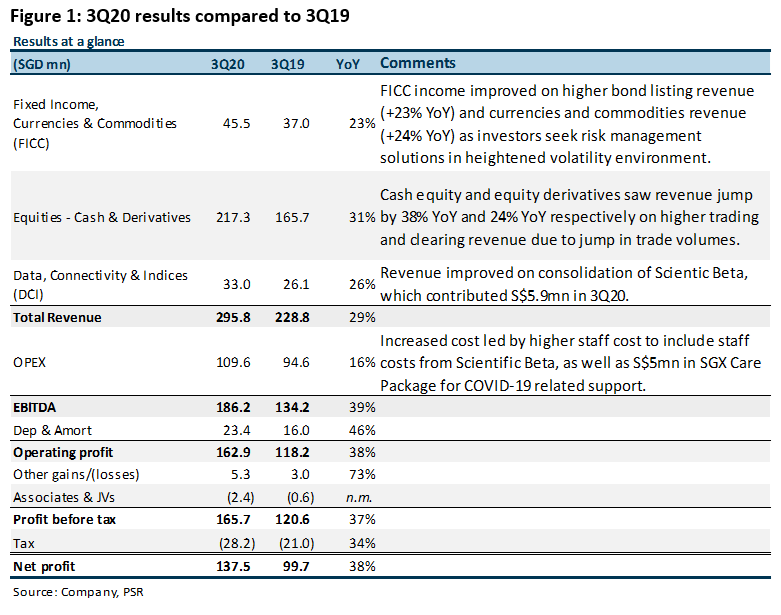

- SGX beat our earnings expectations by 34% for 3Q20.

- Key business segments saw stellar growth amidst heightened market volatility – FICC grew 23% YoY and Equities grew 31% YoY, contributing to a net profit increase of 38% YoY.

- SGX maintained a quarterly dividend of 7.5 cents per share in 3Q20.

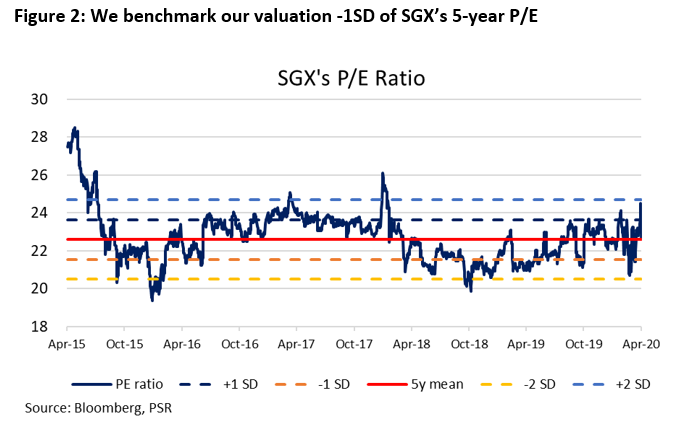

- We maintain our NEUTRAL call with a revised TP of S$9.28. We peg our TP to 21.4x P/E, 1 SD below SGX’s 5-year mean. We revise our FY20e earnings forecast upwards by 8% on stellar 3Q20 results as SGX continues to benefit from market volatility as a result of the COVID-19 pandemic.

The Positives

+ Derivatives business makes a splash in high volatility environment, raking in S$147.5mn, an increase of 24% YoY from S$119mn a year ago. SGX’s effort in developing its derivatives business was also evident, with non-Asian-hour trading activity contributing to 20% of total derivatives volume, a stark increase from less than 10% of total volume from three years ago.

Currencies and commodities derivatives revenue increased 23% with trading and clearing revenue chalking up S$28.8mn, an improvement of 29% YoY on higher volumes. Currency and commodities futures recorded 14.8mn contracts, an increase of 38% across the same period last year.

Revenue increased 24% from equities derivatives, led by higher trading and clearing revenue of S$65.0mn (+26% YoY from $51.6mn) from a 24% increase in trading volume to 61.5mn contracts (3Q19: 49.5mn contracts). Among which, SGX saw higher interest in Nikkei 225 MSCI Taiwan and Nifty 50 index futures (+85%, +44% and +39% YoY respectively).

+ Cash equities business enjoy revitalised interest from dormant retail investors. SGX noted an increase of 50% in accounts that traded in March alone which had no trading activity for the past one year. This propelled a 58% increase in SDAV YoY to S$1.61bn in 3Q20, leading to a 65% increase in trading and clearing revenue to S$67.9mn from S$41.1mn YoY. Settlement and depository management revenue also improved 21% from S$21.4mn to S$25.8mn as a result.

+ Consolidation of Scientific Beta contributed to growth in the DCI business, adding S$5.9mn to the segment as DCI revenue grew 26% YoY from S$26.1mn to S$33.0mn.

The Negatives

– Equity listing and corporate actions revenue fell 4% YoY on poorer market sentiments. While primary and secondary funds raised in the first three quarters exceeded entire FY19 (primary listing: S$2.2bn vs FY19 of S$1.7bn and secondary listing: S$7.6bn vs FY19 of S$4.7bn), capital-raising activity is expected to slump on weaker market valuations in the current climate.

Outlook

The persistence of the COVID-19 will continue to heighten market volatility and benefit SGX’s business. In 3Q20, SGX observed large amounts of funds from institutional investors exiting the market that was matched by fresh funds from retail investors. However, the large amount of fresh funds invested into the bourse is unlikely to be sustainable in subsequent quarters with April’s SDAV standing at around 30% of March’s heightened level.

Investment Actions

We maintain our NEUTRAL recommendation with an upward revision of our TP to S$9.28 on a stellar 3Q20 earnings. Our TP is pegged to 21.4x P/E, 1 SD below SGX’s 5-year mean. Quarterly interim dividend held consistent at 7.5 cents per share also leads to lesser attractiveness in terms of yield (c.3.4%).

Source: Phillip Capital Research - 27 Apr 2020

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Trade Confidently & Analyze Charts Conveniently - Download VCPlus IOS & Android App Now!

Latest Videos

Apps

Top Articles

1

CEO Morning Brief

2

CEO Morning Brief

DBS Shares’ 43% Rally Seen Having More Legs as Wealth Fees Rise

3

CEO Morning Brief

Singapore Post Shares Slide After CEO Fired Over Whistleblower Report

4

5

Johor house best buy

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....