Trader Hub

Frasers Centrepoint Trust – Primed and Awaiting Imminent Growth

traderhub8

Publish date: Fri, 25 Oct 2019, 03:37 PM

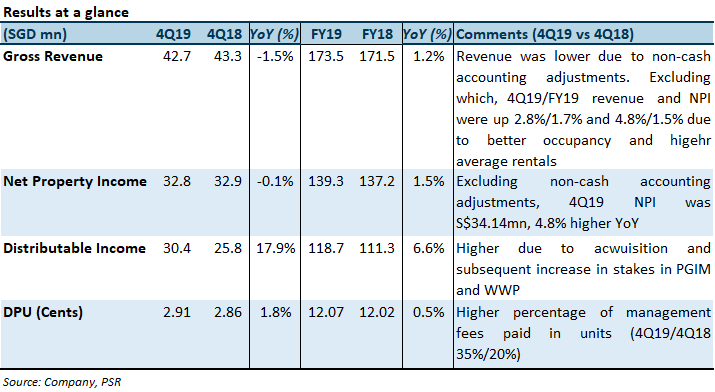

- 4Q19 and FY19 NPI and DPU in line with our forecast.

- Positive rental reversions, higher footfall and increase in FY19 revenue (excluding non-cash accounting adjustments).

- Growth catalysts include FCT’s pipeline assets, intensification of Woodlands and Punggol will benefit CWP and WWP, renewed strength in fringe retail rents and possible acquisition of PGIM’s assets.

- Maintain ACCUMULATE with higher TP of S$3.11 (prev. S$2.77). Higher target price due to the addition of the 6.7% stake in Waterway Point and FCT’s increased stake in PGIM.

The Positives

+ Positive rental reversions of 4.8% for FY19 (FY18 +3.2%). Highest reversions registered at Causeway Point (CWP) (+7.4%), FCT’s largest contributor to revenue. Reversions for the rest of the assets ranged from -1.4% to 2.2%.

+ Shopper traffic up 8.9% in 4Q19 while tenant sales came in flat. Northpoint City North Wing (NPNW), Changi City Point (CCP) and Waterway Point (WP) registered growth in tenant sales between 2% to 6%. However, this was offset by lower tenant sales at due to business disruptions at CWP (partial closure of basement due to underground pedestrian link (UPL) works) and Anchorpoint (changes in anchor tenant).

The Negatives

– Occupancy slipped 0.3ppts QoQ to 36.5%. Causeway Point’s occupancy was 97.0%, lower compared with 98.4% last year due to the ongoing works relating to the construction of the UPL link at its basement level, which is expected to complete in December 2019. Anchorpoint’s occupancy currently at 79.0%, is expected to improve to 94.2% when the new tenants complete their fitting-out progressively in October and November 2019.

Source: Phillip Capital Research - 25 Oct 2019

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Trade Confidently & Analyze Charts Conveniently - Download VCPlus IOS & Android App Now!

Latest Videos

Apps

Top Articles

1

CEO Morning Brief

Keppel DC REIT Buys Data Centres in Singapore’s Genting Lane for S$1b

2

3

CEO Morning Brief

Marina Bay Sands Eyes Singapore’s Largest Loan of US$9b — Bloomberg

4

CEO Morning Brief

WeWork Gives Up Singapore Locations in Sign of Co-working Woes

5

RHB Investment Research Reports

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....