Trader Hub

Penguin International Ltd – Waddling Is Normal

traderhub8

Publish date: Tue, 21 May 2019, 11:42 AM

- Revenue is historically volatile and lumpy. No changes to our earnings forecast.

- Jump in inventories, non-financial liabilities and asset held for sale point to a healthy outlook.

- Balance sheet still in net cash position of S$43.8mn, or 45% of the market capitalisation.

- Our BUY recommendation and target price of S$0.61 remain unchanged.

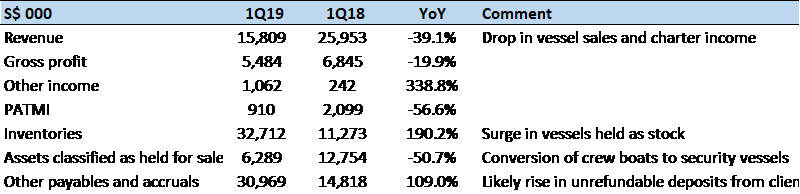

Results at a glance

Source: Company, PSR

The Positives

+ Inventory is up 3x YoY, and assets for sale of S$6.3mn emerges. This was because the company builds vessels to stock; there are two ways to interpret the spike in inventories. It is either the company is now burdened with unordered vessels, or there will be significant recognition of sales in coming quarters. We take the later view due to the rebound in sales last year and improvement in offshore oil and gas activity. Assets for sale was S$6.3mn compared to nil as at end December. It implies the company is converting its crewboat vessel(s) into security vessels for sale. The company does not disclose its order-book. Movements in the balance-sheet will provide a guide to the near term outlook.

+ Net cash of S$43.8mn with the rise in operating cash-flows. The company exited end-March 2019 with net cash of S$43.8mn, a marginal improvement from S$41.6mn as at end 2018. In 1Q19, cash from operations jumped by S$11.6mn due to better working capital.

+ Other payables and accruals doubled YoY and rose S$7.1mn QoQ. Another indicator on the balance sheet that can be an indicator of the future outlook will be the rise in other payables and accruals. Part of the liabilities inside this line item includes advance payments and deposits received from the customer that are not refundable. While not separately disclosed, we believe the S$7mn rise QoQ is in part from deposits received.

The Negatives

– Less charter income in the near-term. Revenue was down 39% YoY in 1Q19. Charter income was not disclosed. However, the earlier mentioned conversion of crewboats to security vessels would have reduced the number of vessels available for charter. Separately, there was a large $9.3mn capex this quarter. The company mentioned this was to expand its operating fleet. As a result, we expect charter income to recover in the following quarters.

Outlook

Historically, revenue is very lumpy and volatile for the company (Figure 1). Over the past three years, revenues have swung from S$6mn to $41mn per quarter. Sale of vessels in the inventory and progress recognition of vessels under contract will not be not even every quarter. There is no change in our positive outlook for the company. As per our initiation report, the three drivers to growth are the revival in offshore oil and gas activities, increased market share and the successful diversification outside the core crewboat and security vessels.

Source: Phillip Capital Research - 21 May 2019

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Trade Confidently & Analyze Charts Conveniently - Download VCPlus IOS & Android App Now!

Latest Videos

Apps

Top Articles

1

CEO Morning Brief

2

Johor house best buy

3

STE's Stocks Investing Journey

4

CEO Morning Brief

DBS Shares’ 43% Rally Seen Having More Legs as Wealth Fees Rise

5

CEO Morning Brief

Singapore Post Shares Slide After CEO Fired Over Whistleblower Report

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....