Trader Hub

SATS Ltd – Eyes Set on Growth Abroad

traderhub8

Publish date: Tue, 21 May 2019, 11:40 AM

- FY19 net income was in line with our expectations.

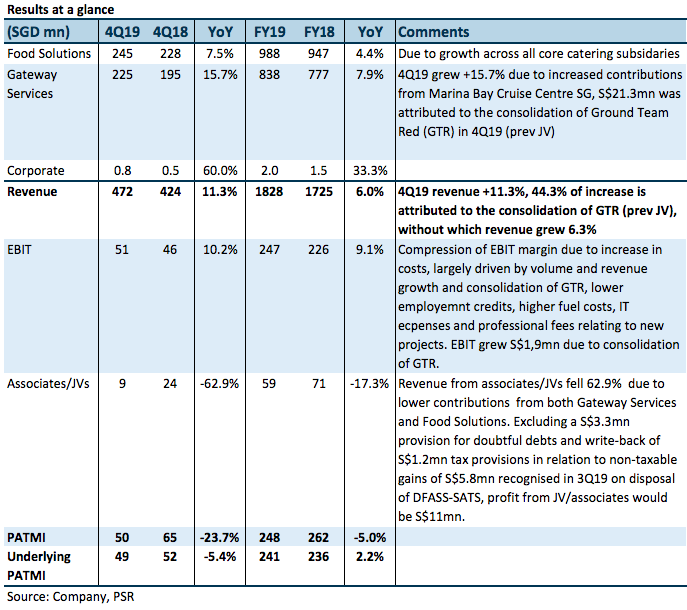

- Food Solutions and Gateway Services revenue grew 4.4% and 7.9% YoY, with growth showing in both Aviation (+11.7%) and Non-Aviation (+8.8%) industries.

- Deepening presence in China through accretive acquisitions

- Food and cargo volumes at Brahims and PT CAS remain flat.

- Maintain ACCUMULATE; unchanged target price of $5.47.

The Positives

- Food Solutions and Gateway Services revenue grew 4.4% and 7.9% YoY with growth showing in both Aviation (+11.7%) and Non-Aviation (+8.8%) industries. Higher food revenue due to increased meal volumes across all core catering subsidiaries while Changi Airport Terminal 4 operations and cruise terminal operations at Marina Bay Cruise Centre Singapore (MBCCS) increased gateway services revenue.

- Deepening presence in China through accretive acquisitions. Acquisition of 50% stake in Nanjing Weizhou Airline Food Corp (NWA) for S$31.2mn. Located in Jiangsu Province near Shanghai, NWA operates on the same strategy as STAS, using central kitchen to supplement flight kitchens. NWA has a network of 12 cold storage facilities/distribution channels; enabling it to serve 80 airports domestically. Using our FY20e P/E assumption of 24x, the deal could add c.S$1.3mn to SATS’ bottom line.

The Negatives

- Food and cargo volumes at Brahims and PT Cas remain flat. Cargo volumes were dampened by the ongoing trade tensions. Management commented that they have managed to pass on most of the concession and price increases and rationalisation efforts have yielded improvements in efficiency.

Outlook

The outlook is positive. Passenger traffic growth is expected to drive volume growth while digitalisation efforts will provide efficiency and productivity gains to cope with pricing pressure from airlines. Renewal of contract with SIA on 5+5 years terms covers the majority of the revenues from SIA and will provide more certainty of margins and pricings moving forward.

SATS’ continues to pursue growth opportunities in China. Investments in the central kitchen allow them to fulfil the demand from fast casual restaurant chains in key cities while supplementing shortfalls in-flight kitchen. The expectation of volume growth is driven by aviation demand and demand for quality food.

Potential risk factors include challenges arising from trade tensions impacting cargo volumes and airline pressure from fuel costs.

Source: Phillip Capital Research - 21 May 2019

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

CEO Morning Brief

2

Johor house best buy

3

STE's Stocks Investing Journey

4

CEO Morning Brief

DBS Shares’ 43% Rally Seen Having More Legs as Wealth Fees Rise

5

CEO Morning Brief

Singapore Post Shares Slide After CEO Fired Over Whistleblower Report

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....