Trader Hub

Singapore O&G Ltd. – Ceasing Coverage

traderhub8

Publish date: Thu, 21 Feb 2019, 07:40 PM

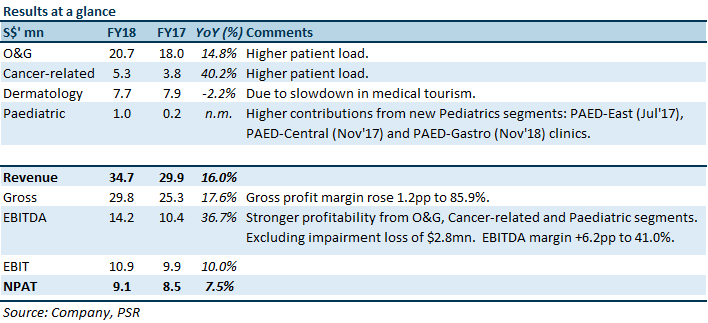

- FY18 Revenue exceeded our full year expectations by 7%. Adjusted PATMI met our full year estimations (excluding settlement fee receipt and legal fees from the dispute and impairment of goodwill).

- O&G and cancer-related segments were the star performers, rising 15% YoY and 40% YoY respectively.

- Dermatology continues as a drag to group earnings, contracting 2% YoY due to the slowdown in medical tourism.

- Added one paediatrician and one dermatologist in FY18. Total number of specialists in FY18 at 14 (FY17: 12 specialists).

- Proposed final dividend of 0.90 cents/share. FY18 dividend per share: 1.70 cents (FY17: 1.50 cents).

- Ceasing coverage due to reallocation of internal resources.

The Positives

- Significant improvement in EBITDA, due to the pick-up in profitability of O&G, cancer related and paediatric segments. The O&G segment delivered 1,824 babies in FY18 as compared to 1,716 in FY17, growing 6% YoY (FY17: -1% YoY). As more specialists inch towards their breakeven point even though the total number of O&G specialists remained flat at 6. It typically takes 1-2 years for specialists to breakeven.

- Cancer-related segment revenue grew 40% YoY, more than offset the challenging dermatology segment and gestations costs incurred by the newly established paediatrics segment.

The Negatives

- Dermatology segment performance lacklustre due to a slowdown in medical tourism. FY18 EBIT declined 5% YoY, and EBIT margin fell 0.9pps to 29.7%. The number of patients treated by Dr Joyce Lim was reduced because of the slowing medical tourism and her active involvement in teaching and conferences to gain visibility. In a bid to expand the dermatology business, SOG recruited one new dermatologist in December 2018 who specialises in paediatric dermatology.

- The new Paediatrics segment incurred S$0.5mn ‘start-up’ losses to date. One new paediatrician joined in November 2018. We expect the two existing Paediatricians to breakeven by end-FY19. The two paediatricians joined in July and November 2017.

- S$2.8mn impairment of goodwill. The impairment relates to the excess of the carrying amount of the cash generating unit (CGU) over the recoverable amount of the CGU as at year end of the Dermatology segment, using a DCF valuation model and projected over 7 years plus terminal value. Current accounting standards require impairment instead of

Outlook

With a gradual recovery in birth rates in Singapore, coupled with the Group’s ability to consistently gain market share in live births in Singapore, we expect the O&G segment to continue registering better growth.

We also expect the cancer-related segment to support Group’s FY19e profitability amidst persistent headwinds – (a) sluggish birth rate and (b) structural slowdown in medical tourism.

Profitability from the O&G and Cancer-related segment should improve as more doctors breakeven and gain more patient load. The Group is actively seeking suitable doctors to join its team to further grow its four business pillars. New doctors typically take 1 – 2.5 years to break even.

The Group has a robust balance sheet with zero debt and a cash position of S$21.5mn (c.13% of its market cap).

Ceasing coverage

Our most recent rating from our 13 August 2018 report, was Buy with a target price of $0.420. We are ceasing coverage on this counter due to the reallocation of internal resources.

S$1.25mn non-recurring item booked in 2Q18Refer to the announcement dated 6 Mar-18, SOG has received the settlement amount of S$1.25mn for a settlement related to a dispute with its former Lead Independent Director, Mr. Christopher Chong Meng Tak.

Source: Phillip Capital Research - 21 Feb 2019

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

RHB Investment Research Reports

2

Collin Seow Remisier Blog

3

THE SINGAPOREAN INVESTOR

Frasers Centrepoint Trust's Annual Report for FY2023/24 - Key Highlights to Take Note of

4

CEO Morning Brief

5

CEO Morning Brief

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....