Trader Hub

Thai Beverage PLC – a Spirited Recovery

traderhub8

Publish date: Tue, 19 Feb 2019, 09:41 AM

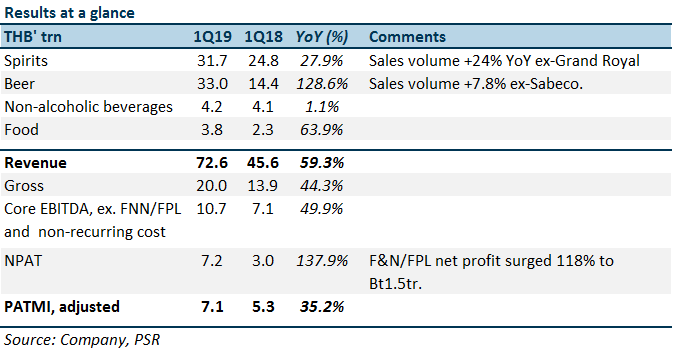

- Revenue and EBITDA were above expectations but was offset by higher than expected interest expense and weaker earnings from Sabeco.

- Recovery in spirits volume was better than expected despite moderate improvement in farm income. Thailand rice aid scheme has boosted farm incomes.

- Upgrade to NEUTRAL and increased our SOTP-derived TP to S$0.81 (previously S$0.57). Our aggressive upgrade in share price is due to: (i) We raised our earnings by 7% as we expect demand to remain vibrant over the next few quarters; (ii) We raised our SOTP valuation to the middle (from lower) EV/EBITDA band of global peers.

The Positives

+ Domestic spirits volume is up 24% YoY. Demand for spirits in Thailand surged 24%. The rise was in part due to low base after the imposition of excise tax on September 2017. This lead to front-loading of purchases in 4Q17 and reduced buying in subsequent 1Q18. Excluding the lower base, there was a recovery in demand. More impressive was volume growth in Grand Royal whisky (Myanmar). Volumes surged 36% YoY and there is no base effect.

+Upside surprise in F&N/FPL earnings. Net profit contribution from F&N and FPL surged 118% YoY to Bt1.5t. F&N enjoyed a recovery in dairy business and FPL benefited from strong sales in Australian residential properties.

The Negatives

– Sabeco still not contributing much. Despite the consolidation of Sabeco financials and the 128% YoY surge in revenue for the beer segment, net profit for this division actually fell 54% YoY. The bulk of the 117% spike in EBITDA for beer segment was offset by the jump in interest expenses.

– Missing minority interest. There was minimal minority interest in this quarter’s results despite Sabeco consolidation. In comparison, 3Q18-4Q18 minority interest was between Bt345mn and Bt656mn. This was down to Bt64mn. The explanation given was the transition from Vietnam to Thailand accounting standards plus the recognition of bonus and social welfare fund. The size was not disclosed.

Outlook

We believe there is sales momentum for the company in the coming 2-3 quarters, in particular for the spirits business that accounts for 75% of net earnings. Firstly, there is the “customary” boost in consumption in pre-election campaigning. Secondly, assuming election are peaceful, there will be grand events and celebration for the new posts. Thirdly, the coronation of new King in May will create a celebratory atmosphere, unlike the past two years. Finally, additional farm aid for rice farmers will boost their income levels especially in Southern Thailand (refer below).

Where our assumptions were wrong?

While the share price did come close to our target price of S$0.57, the turnaround in the business was much faster than anticipated. We had expected a modest recovery in farm income based on our reading of the Thailand Farm Income Index. However, the rebound in farm income was better than expected. This was in large part due to the rolling out of Bt56.5bn farm aid scheme for rice farmers that began in late Oct18. This would boost farm incomes by around Bt13,800 per farmer. This is a significant amount since average farm incomes in Thailand are Bt57,000 per annum. Another Bt5bn has been allocated for farmers in the South. This will run until Jun/Jul19.

Raised to NEUTRAL and SOTP-derived TP of S$0.81 (previously S$0.57)

Upgrade to NEUTRAL and increased our SOTP-derived TP to S$0.81 (previously S$0.57). Our aggressive upgrade in share price is due to: (i) We raised our earnings by 7% as we expect demand to remain vibrant over the next few quarters; (ii) We raised our SOTP valuation to the middle (from lower) EV/EBITDA band of global peers.

Source: Phillip Capital Research - 19 Feb 2019

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Trade Confidently & Analyze Charts Conveniently - Download VCPlus IOS & Android App Now!

Latest Videos

Apps

Top Articles

1

RHB Investment Research Reports

2

Collin Seow Remisier Blog

3

THE SINGAPOREAN INVESTOR

Frasers Centrepoint Trust's Annual Report for FY2023/24 - Key Highlights to Take Note of

4

CEO Morning Brief

5

CEO Morning Brief

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....