Trader Hub

M1 Limited – ARPU Pressure Offset by Subscriber Growth

traderhub8

Publish date: Wed, 30 Jan 2019, 04:43 PM

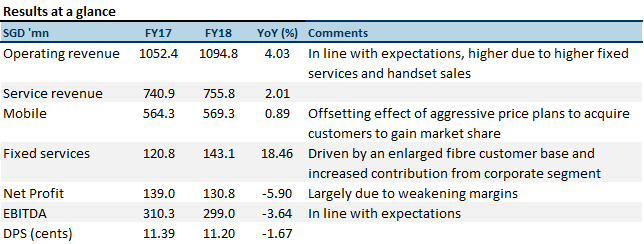

- Overall results are in line with our expectations

- Full year dividend of 11.2 cents, a mild 2% contraction from a year ago

- ARPU contracted 4.3% YoY in 4Q18 but was offset by subscriber growth of 7.1%. Post-paid subscribers rose a record 92k.

- We maintain our NEUTRAL recommendation with an unchanged TP of S$2.06. Shareholders should accept the VGO.

Source: Company, PSR

The Positives

+ Healthy growth in fixed services. Higher fixed services revenue contributed by increased fibre customer base and corporate projects. Fibre customer base increased to 209,000 or 10.6% YoY. M1 is gaining traction in corporate projects.

The Negatives

– Lowered ARPU for market share. M1 and its Mobile Virtual Network Operator (MVNO) partner Circles.Life have been able to secure post-paid market share with their aggressive price plans. Post-paid subscribers gained 92,000 or 7.12% YoY in 2018. This is the largest rise in subscriber in more than 10 years. ARPU decline 4.3% in 2018, in part due to the wholesale pricing offered to MVNOs. Another reason for lower ARPUs is to prepare for the impending entry of TPG Telecom this is done to lock in customers in the post-paid segment. Assuming that all post-paid contract tenure is 2 years, M1 managed to secure 137,000 subscribers who are unlikely to switch to TPG due to potential penalties imposed.

ACCEPT THE VGO

We view the VGO as an opportunity for shareholders to realise their investments at a premium to current market price. M1 is undoubtedly the most exposed to the entrance of TPG and increased competition from the rise of more MVNOs. 80% of revenue is derived from the Singapore mobile market. Close of the offer is on 4 February 2019.

Maintained NEUTRAL recommendation with an unchanged target price of S$2.06

We maintain our NEUTRAL recommendation with an unchanged target price of S$2.06. We think shareholders should accept the VGO offer at S$2.06.

Source: Phillip Capital Research - 30 Jan 2019

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Trade Confidently & Analyze Charts Conveniently - Download VCPlus IOS & Android App Now!

Latest Videos

Apps

Top Articles

1

RHB Investment Research Reports

2

Collin Seow Remisier Blog

3

THE SINGAPOREAN INVESTOR

Frasers Centrepoint Trust's Annual Report for FY2023/24 - Key Highlights to Take Note of

4

CEO Morning Brief

5

CEO Morning Brief

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....