Trader Hub

Micro-Mechanics (Holdings) Ltd – 2018 a Difficult Comp

traderhub8

Publish date: Wed, 30 Jan 2019, 04:42 PM

- Revenue and PATMI were below our expectations. We are lowering our FY19e revenue and PATMI by 5% and 12% respectively.

- Top-line has been hurt by a general slowdown in semiconductor demand, exarcebated by uncertainty over trade talks between US and China.

- In-line with our lower earnings estimate, we have reduced our target price on MMH to S$1.70 (previously S$2.05). We peg our valuations to 15x FY19e PE. This is in-line with back-end semiconductor supply chain valuations. We lowered our recommendation to ACCUMULATE.

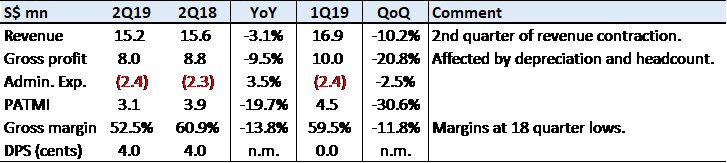

Results at a glance

Source: Company, PSR

The Positives

+ U.S. operations still enjoying healthy growth. The revenue in the U.S. grew 8% YoY in 2Q19. This division targets front-end semiconductor equipment parts. It will be the next major leg of growth after the current back-end segment. However, little was shared in terms of projects or programmes.

The Negatives

– Gross margins the weakest since 4Q14. GP margins fell to 52.4%, the weakest in 18 quarters. We assume the weak margins was due to customer pricing pressure, higher production headcount and the rise in depreciation after last year’s lumpy S$12mn capex. Depreciation rose 15% YoY in 2Q19.

– Revenue dragged by China. Revenue in 2Q19 contracted for the second consecutive quarter. Revenues from MMH largest division, China , fell by 7% YoY. Uncertainty over trade negotiations between the U.S. and China has created caution in the supply chain and hesitation in carrying inventory.

Outlook and Recommendation

The revenue slowdown has been steeper than expected. 2018 was a bumper year due to the surge in memory semiconductors. The core competitiveness of the company has not changed. MMH provides customized (and even the single source) consumables for the die attach process. As wafer circuitry shrink to nanometers, it will increase the fragility and electrostatic discharge sensitivity of the die. MMH strength is their ability to constantly ride the technological wave together with their customers and resolve their ever-present challenges. We lowered our recommendation to ACCUMULATE on MMH. The company maintains one of the highest gross margins and ROE in the semiconductor back-end industry. Our target price of S$1.70 (previously S$2.05) is based on 15x FY19e PE. This is in-line with back-end semiconductor supply chain valuations. MMH pays an attractive dividend yield of 6% as we wait for the semiconductor cycle to recover.

The report is produced by Phillip Securities Research under the ‘SGX StockFacts Research Programme’ (administered by SGX) and has received monetary compensation for the production of the report from the entity mentioned in the report.

Source: Phillip Capital Research - 30 Jan 2019

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

RHB Investment Research Reports

2

Collin Seow Remisier Blog

3

THE SINGAPOREAN INVESTOR

Frasers Centrepoint Trust's Annual Report for FY2023/24 - Key Highlights to Take Note of

4

CEO Morning Brief

5

CEO Morning Brief

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....