Trader Hub

China Sunsine Chemical Holdings Ltd – Still Healthy Performance

traderhub8

Publish date: Fri, 09 Nov 2018, 10:14 AM

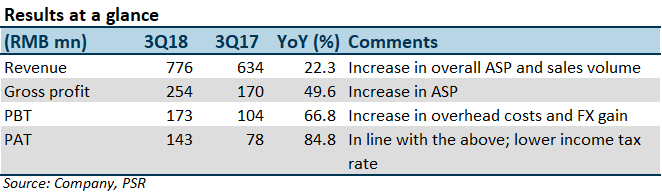

- 3Q18 revenue and net profit exceeded our full year expectation due to higher ASP and GPM.

- Both GPM and NPM remain at record levels.

- ASP corrected since 2Q18.

- New capacity delayed and approval still pending.

We revise up FY18e EPS by 17.5% to 26.9 SG cents and FY19e EPS by12.7% to 23.9 SG cents. Due to expected softer ASP, the required rate of return was changed from 8% to 10% based on an updated Beta. We maintained our BUY recommendation with a lower target price of S$1.68.

Positives

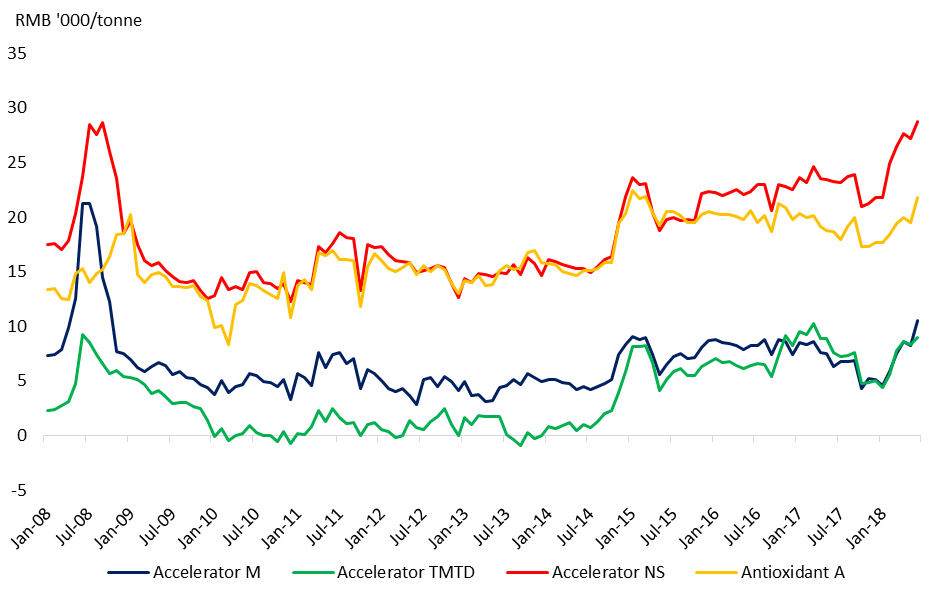

+ Both GPM and NPM remain at record levels: 3Q18 GPM and NPM arrived at 32.7% and 18.5% respectively, comparing to GPM of 26.8% and NPM of 12.2% in 3Q17. Accordingly, 9M18 GPM and NPM achieved 34.9% and 21.2% (Strip out one-off credit of tax expense of RMB48mn, and adjusted NPM is 19.3%). The phenomenal margins are due mainly to the widened spread between ASP and cost of raw materials (major material: aniline) within the market, see Figure 1.

Figure 1: Price spread (accelerator/antioxidant and aniline)

Source: CEIC, PSR

Negatives

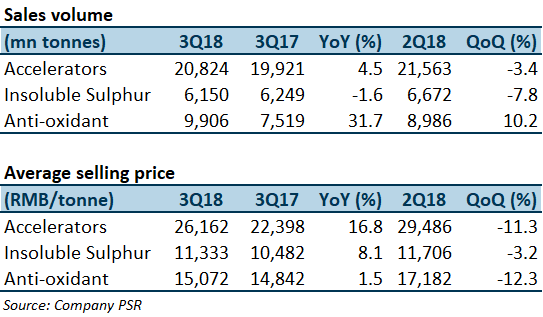

– ASP corrected since 2Q18: 3Q18 performance turned to be the worse quarter out of the recent four in terms of top and bottom line due to a price correction. The overall 3Q18 ASP was RMB20.7k/tonne (4Q17, 1Q18, and 2Q18: RMB22.4k/tonne, RMB23.2k/tonne, and RMB23.3k/tonne). The decrease was the result of both softer raw material prices and demand for tyre.

– New capacity delayed and final approval still pending: The approval of the trial run of the respective 10k-tonne newly-added capacity of accelerator TBBS and insoluble sulphur plant was postponed again (previously management expected to get by 3Q18). The current status was at the final stage.

Outlook

CSSC is facing a bit headwind of ASP correction currently. However, we believe there is a limited downside since overall supply within the market has not increased substantially. At the moment, the dip in both finished products and materials resulting from softened demand is cyclical. We ought to concentrate on the ramp-up of capacity and production which will be realised in the near term. We still expect 4Q18 GPM to sustain at above 30%. As of 3Q18, cash in hand reached RMB822mn, and we expect it to reach more than RMB1bn in FY18. It is beneficial to hoard cash when the market is in favour of business, preparing for future development when the market turns.

Maintain BUY with a lower TP of S$1.68

We revise up FY18e EPS by 17.5% to 26.9 SG cents and FY19e EPS by12.7% to 23.9 SG cents. Due to expected softer ASP, the required rate of return was changed from 8% to 10% based on an updated Beta. We maintained our BUY recommendation with a lower target price of S$1.68.

Source: Phillip Capital Research - 09 Nov 2018

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

RHB Investment Research Reports

2

Collin Seow Remisier Blog

3

THE SINGAPOREAN INVESTOR

Frasers Centrepoint Trust's Annual Report for FY2023/24 - Key Highlights to Take Note of

4

CEO Morning Brief

5

CEO Morning Brief

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....