Trader Hub

Ascendas REIT: Acquired Second UK Portfolio

traderhub8

Publish date: Fri, 26 Oct 2018, 10:50 AM

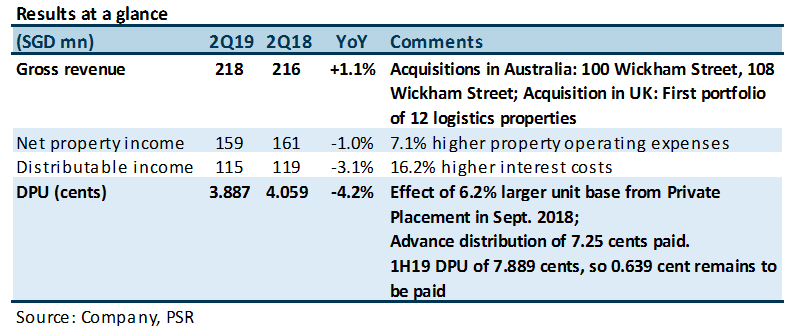

- Gross revenue and DPU were within expectation

- Acquisition of the second UK portfolio was completed on Oct. 4, subsequent to 2Q19

- Maintain Accumulate; new target price of $2.78 (previous $2.82)

The Positives

- Positive rental reversions across all segments in Singapore. Rental reversions ranged between +0.3% and 3.0% across the five segments. There were no renewals signed in Australia and UK.

- Long WALE of 14.5 years for the UK portfolio mitigates uncertainty of Brexit. The earliest lease expiry in the UK portfolio is in FY22. A-REIT’s total portfolio weighted average lease expiry (WALE) is 4.3 years.

- Higher proportion of borrowings are on fixed rate, thus mitigating interest rate risk.6% of borrowings are on fixed rate, compared to 72.4% in the previous quarter. Meanwhile, all-in debt cost which has risen 10bps QoQ to 3.0%. Average debt maturity has improved QoQ from 3.7 years to 3.2 years.

The Negatives

- Lower Singapore occupancy, mainly due to non-renewals at logistics properties. Singapore portfolio is lower QoQ from 88.1% to 87.1%. The addition of the first UK portfolio (100% occupied) helped to lift A-REIT’s total portfolio occupancy marginally by 0.1pps to 90.6%. Australia occupancy was marginally lower QoQ by 0.1pps to 98.5%.

- Expect aggregate leverage to increase due to the second UK portfolio. Current leverage of 33.2% is lower than previous quarter’s 35.7% due to the Private Placement. However, we estimate leverage to rise to 36.4% by the end of FY19, due to the acquisition of the second UK portfolio that was completed on Oct. 4.

Outlook

The outlook is mixed. Singapore occupancy likely to continue being under pressure, as existing supply has to be absorbed. Total portfolio faces 4.4% of expiry by gross rental income in 2H FY19, almost entirely in Singapore. The asset type that is most exposed to renewal risk is Logistics & Distribution Centres (37% of Singapore expiries). Portfolio’s distributable income will grow from the recent acquisitions. However, DPU for the next three quarters is expected to be lower YoY, due to the effect of the Private Placement.

Maintain Accumulate; new target price of $2.78 (previously $2.82)

Lower target price as we temper our expectation on rental growth for the Singapore portfolio. Nonetheless, we expect the yield of ~6% to remain stable and our target price gives an implied 1.30 times FY19e forward P/NAV multiple.

Source: Phillip Capital Research - 26 Oct 2018

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

Johor house best buy

HEXCAP (0035) TRANSGRID VENTURES VERSUS MN HOLDINGS: Compare & Contrast

2

RHB Investment Research Reports

3

Collin Seow Remisier Blog

4

CEO Morning Brief

Singapore Growth Beats Estimates as PM Wong Flags Global Risks

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....