Trader Hub

Dasin Retail Trust: Grounding on Healthy Operating Metrics

traderhub8

Publish date: Wed, 15 Aug 2018, 02:12 PM

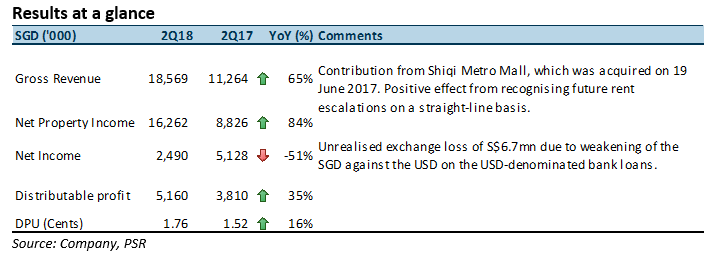

- Revenue in line with and NPI exceeded our expectations for 2Q18. Boost in revenue from the acquisition of Shiqi Metro Mall in June 2017. Organic growth was 10.4% YoY.

- Strong 100% occupancy and well-spread WALE (by GRI) of 4.07 years.

- Increase in gearing due to revaluation of investment properties.

The Positives

+ 10% of leases by GRI were renewed in 1H18, with 12.2% positive reversions and 100% portfolio occupancy. What this tells us is that there is demand for the space, and it is currently under-rented. The WALE has also been lengthened QoQ from 4.01 years to 4.07 years. While the 17.9% of leases (by GRI) that are due for renewal in 2H18 poses some concern, the Manager has proven its ability to execute. As such, we expect positive rental reversions to maintain in 2H18.

The Negatives

– Gearing increased to 31.5% in 2Q18 from 30.4% as at end 1Q18. This was mainly due to the decline in valuation of investment properties, which relates to the lease renewals of anchor tenants at Xiaolan Metro Mall and Shiqi Metro Mall, where the newer rents were lower than those of smaller, non-anchor tenants.

Outlook

Current gearing of 31.5% affords Dasin S$138.6mn of headroom (assuming 40% gearing) to pursue inorganic growth, which will be through its ready pipeline of 20 properties – 12 of which have been completed.

Downgrade to ACCUMULATE with unchanged target price of S$0.97

Fundamentals remain intact, and our target price remains unchanged. Our rating downgrade is purely due to the recent positive price moment.

Source: Phillip Capital Research - 15 Aug 2018

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Trade Confidently & Analyze Charts Conveniently - Download VCPlus IOS & Android App Now!

Latest Videos

Apps

Top Articles

1

RHB Investment Research Reports

2

Collin Seow Remisier Blog

3

THE SINGAPOREAN INVESTOR

Frasers Centrepoint Trust's Annual Report for FY2023/24 - Key Highlights to Take Note of

4

CEO Morning Brief

5

CEO Morning Brief

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....