Trader Hub

China Everbright Water Limited: Stable Expansion

traderhub8

Publish date: Fri, 10 Aug 2018, 04:32 PM

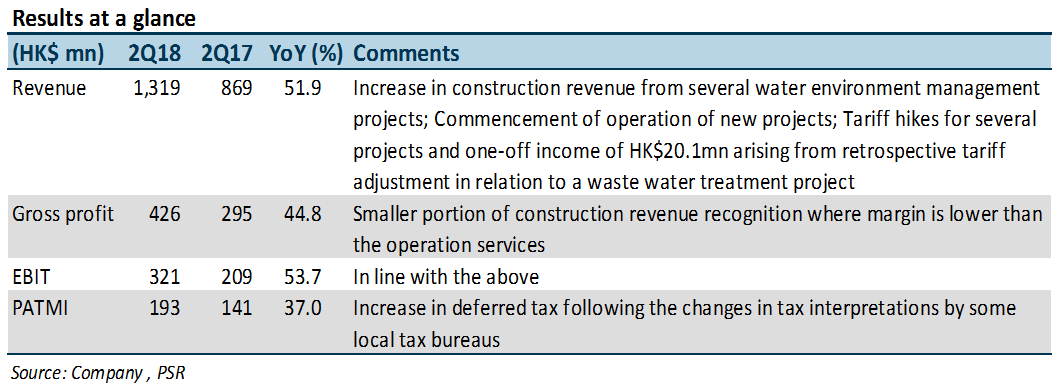

- Both 2Q18 revenue and PATMI met expectations.

- As at Jun-18, CEWL has a portfolio of 100 projects, 86 are operating, 7 under construction and 7 in preparatory

- Ongoing organic growth through tariff hikes and project upgrading.

- The completion of Zhenjiang Sponge city project could be postponed to 2019.

- Expect a higher valuation when being listed Hong Kong.

- We tweaked up FY18e EPS to 5.0 SG cents (previously 4.8 SG cents). We lowered our target price to S$0.53 (previously SG$0.55), due to lower peers’ valuations of 10.6x (previously 11.4x), and maintained a BUY recommendation.

The Positives

+ Ongoing upgrading of projects: In 2Q18, there were six waste water treatment (WWT) projects securing tariff hikes ranging from 1% to 165%, out of which four projects were due to completion of upgrading, and the rest were due to normal tariff upward adjustments. During the period, the group received a one-off HK$20.1mn retrospective tariff adjustment which was a collection of delayed payment due to the Spring Festival in 1Q18.

The Negatives

– Updates of Zhenjiang Sponge City project: Due to some issues on the construction of the pipeline network, completion of the project could be postponed again to 2019 (previously expected to complete by 2018). The group has been working on it and negotiating with the authority. Hopefully, it will speed up the process of inspection and construction.

Outlook

As of 2Q18, the total WWT was above 5mn tonnes/day. It is expected that organic growth based upgrading of the existing projects, will ramp up capacity to 10% to 20% per annum. However, it is still short of the goal of 10mn tonnes daily WWT capacity by 2020. Therefore, the group may seek more project acquisitions. The group continues to prioritise the quality of the project instead of pursuing quantity.

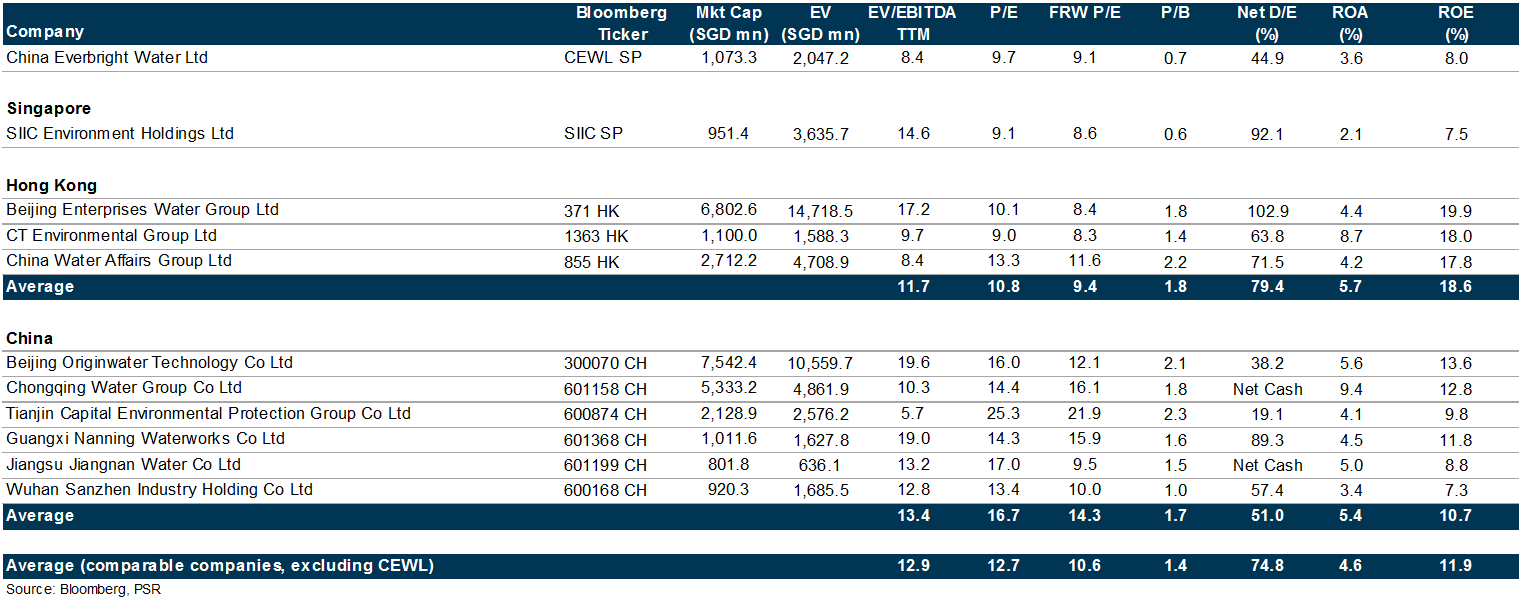

In Aug-18, the group applied for dual listing in Hong Kong. Management thinks Hong Kong investors are more familiar with the WWT business given that a number of peers are listed there. Based on Figure 1, the Hong Kong peers trade at higher price-to-book ratios, but these are in part due to higher ROEs.

Maintain BUY with a lower TP of S$0.53

We tweaked up FY18e EPS to 5.0 SG cents (previously 4.8 SG cents). We lowered our target price to S$0.53 (previously SG$0.55), due to lower peers’ valuations of 10.6x (previously 11.4x), and maintained a BUY recommendation.

Figure 1: Hong Kong peers are valued higher on P/B basis but in part due to their higher ROEs

Source: Phillip Capital Research - 10 Aug 2018

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Trade Confidently & Analyze Charts Conveniently - Download VCPlus IOS & Android App Now!

Latest Videos

Apps

Top Articles

1

RHB Investment Research Reports

2

Collin Seow Remisier Blog

3

THE SINGAPOREAN INVESTOR

Frasers Centrepoint Trust's Annual Report for FY2023/24 - Key Highlights to Take Note of

4

CEO Morning Brief

5

CEO Morning Brief

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....