Trader Hub

Ascendas REIT: Operationally Stable

traderhub8

Publish date: Tue, 31 Jul 2018, 10:52 AM

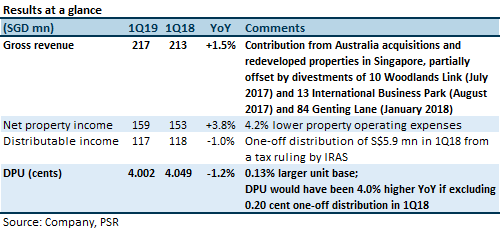

- Gross revenue and DPU were within expectation

- Overall portfolio remains operationally stable

- Lower YoY DPU due to one-off distribution last year

- Maintain Accumulate; unchanged target price of $2.96

The Positives

+ Positive rental reversion of +10.5% for the portfolio. All segments in Singapore experienced positive reversions except for Logistics & Distribution Centres (-6.1%). The highest reversion came from High-Specifications Industrial and Data Centres (+24.8%). There were no renewals in Australia during the quarter.

+ Healthy WALE of 4.1 years that is above sector average of 3.7 years (as at March 31). However, the portfolio weighted average lease expiry (WALE) is slightly lower QoQ from 4.2 years. Singapore WALE stands at 4.0 years, while Australia WALE is 5.0 years.

+ Higher proportion of borrowings are on fixed rate, thus mitigating interest rate risk.4% of borrowings are on fixed rate, compared to 71.9% in the previous quarter. At the same time, average debt maturity has improved QoQ from 3.2 years to 3.4 years. Debt maturity profile is staggered, with a policy of no more than 20% of total debt maturing in any given year.

The Negatives

– Lower portfolio occupancy, led by lower Singapore occupancy. Total portfolio occupancy is lower QoQ from 91.5% to 90.5%. The Singapore portfolio occupancy was lower QoQ from 89.5% to 88.1%. Meanwhile, Australia occupancy improved QoQ from 98.5% to 98.6% due to the acquisition of 169-177 Australis Drive and 1314 Ferntree Gully Drive.

– QoQ higher leverage of 35.7% from 34.4%. Debt headroom is correspondingly lower QoQ from S$1.0 bn to S$0.7 bn. The current debt headroom can potentially grow the AUM by 6.8%.

Outlook

The outlook is stable. The portfolio is sufficiently diversified to cushion any short-term localised impact. The portfolio is seeing organic growth from positive rental reversions, and there is inorganic growth to look forward to from acquisitions such as the recently announced proposed acquisition of a portfolio of 12 logistics properties in the UK.

Maintain Accumulate; unchanged target price of $2.96

We expect the yield of ~6% to remain stable and our target price gives an implied 1.40 times FY18/19e forward P/NAV multiple.

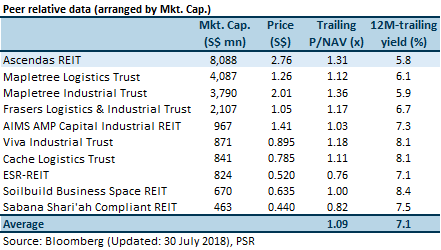

Relative valuation

A-REIT is trading above the peer average P/NAV multiple and at a lower 12M-trailing yield than the peer average.

Source: Phillip Capital Research - 31 Jul 2018

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

RHB Investment Research Reports

2

Collin Seow Remisier Blog

3

THE SINGAPOREAN INVESTOR

Frasers Centrepoint Trust's Annual Report for FY2023/24 - Key Highlights to Take Note of

4

CEO Morning Brief

5

CEO Morning Brief

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....