Trader Hub

Frasers Centrepoint Trust: Steady as She Goes

traderhub8

Publish date: Fri, 27 Jul 2018, 10:29 AM

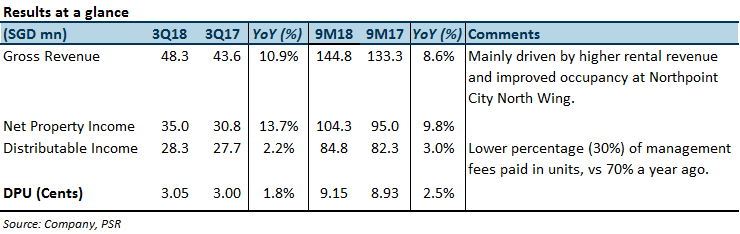

- 9MYTD NPI and DPU were in line with our forecast, at 75% of our FY18e forecast.

- Northpoint City North Wing (NPNW) main growth driver for portfolio occupancy and positive portfolio rental reversion.

- Percentage of debt hedged on fixed rates increased to 64% with all-in cost of debt maintained at c.2.5%.

- Maintain Neutral with higher TP of S$2.15 (prev. S$2.14).

The Positives

+ Overall portfolio occupancy stable at 94% as NPNW continues to fill up post-AEI. Occupancy at NPNW currently at 95.2%, compared to pre-AEI level of 65.9% a year ago, and is expected to improve to 97% by the end of FY18 after factoring in pre-committed leases. Changi City Point had also seen improved occupancy, from 90.6% to 92.6% QoQ.

+ Overall rental reversion maintained at 5% driven largely by NPNW. Portfolio rental reversion of 5% on par with FY17 rental reversions. A tenant within the financial institution sector had taken over a large lease next to its existing space, which was initially due for renewal during the quarter. The renewed lease accounted for c.50% of NPNW’s renewed NLA and was the main driver for the mall’s +25.8% rental reversion in 3Q18.

+ Increased percentage of debt hedged while keeping all-in cost of debt in check. Subsequent to the quarter, FCT had increased its proportion of debt on fixed interest rates to 64% (30 Jun 2018: 55%) while keeping all-in cost of debt largely in check, at 2.5%.

The Negatives

– Tenant sales was lower YoY overall in the single-digit percentage range, excluding NPNW and CCP. NPNW and CCP lifted portfolio tenant sales to 3.4% YoY. There has not been any YoY improvement in tenant sales at the other malls for two quarters. Portfolio occupancy cost has crept up to 16.3% from 15.3% in FY15, in part due to NPNW’s AEI. We opine that tenant sales would need to catch up fast enough to ensure sustainable rental growth.

Outlook

FCT will deploy S$15mn to develop an underpass linking Causeway Point to the upcoming Woods Square. Works will last from end-February 2019 to December 2019 and space carved out for this walkway will be retained under FCT’s reserve GFA bank for future expansion. While there will be a temporary dip in occupancy during this period, the underpass will bring about improved connectivity and expand the catchment area for Causeway Point (48% of portfolio NPI).

Maintain NEUTRAL with higher TP of S$2.15 (prev S$2.14)

Our target price translates to a FY18e yield of 5.4% and a P/NAV of 1.11. There have been adjustments on assumptions on rental reversion rates and financing costs, following a change in analyst.

Source: Phillip Capital Research - 27 Jul 2018

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Trade Confidently & Analyze Charts Conveniently - Download VCPlus IOS & Android App Now!

Latest Videos

Apps

Top Articles

1

RHB Investment Research Reports

2

Collin Seow Remisier Blog

3

THE SINGAPOREAN INVESTOR

Frasers Centrepoint Trust's Annual Report for FY2023/24 - Key Highlights to Take Note of

4

CEO Morning Brief

5

CEO Morning Brief

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....