Trader Hub

CNMC Goldmine Holdings Limited: Satisfactory CIL Results

traderhub8

Publish date: Thu, 17 May 2018, 05:05 PM

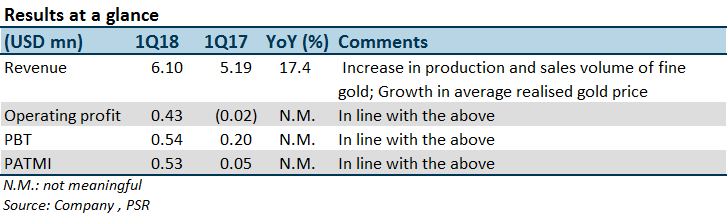

- Revenue and net profit exceeded expectations due to contribution from the Carbon-in-leach (CIL) plant.

- The first gold pour from CIL plant delivered a substantial improvement in production.

- Business remains intact under the new federal administration.

- Both operating and non-operating costs will surge.

- We revise up FY18e and FY19e EPS to 1.9 US cents and 2.7 US cents (previously 1.3 US cents and 1.7 US cents) due to the substantial improvement from CIL plant which will be operational in 2Q18. We upgrade our recommendation to BUY with a higher TP of S$0.42 as we expect production and earnings will rebound strongly this year.

The Positives

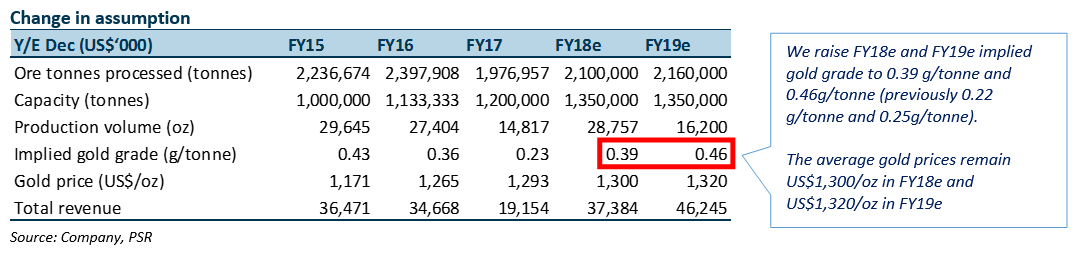

+ The first gold pour from CIL plant delivered a substantial improvement in production. In Apr-18, the Group announced the first gold pour arrived at 863.3oz because of 2 weeks operation in Mar-18. Based on the daily ore processing capacity of 500 tonnes, the implied ore grade range from 3.1g/tonne to 3.5g/tonne. By contrast, the implied ore grade from the existing plants (heap leach and vat leach) was 0.23g/tonnes as of Dec-17. The cut-off grade for CIL operation is expected to be 1g/tonne. Currently, the Group has conserved a certain amount of high-grade ores specifically for CIL. Meanwhile, management is confident to extract ores that are above the cut-off grade to keep CIL plant’s operation smoothly in a few years.

+ Business remains intact under the new federal administration. The core officials of Kelantan state government was unchanged. The large change is at the federal administration. The key concessions such as exploration royalties have been renewed years ago. Hence, the Sokor field projects will continue operations without any change.

The Negatives

– Both operating and non-operating costs will surge. The group increased manpower and procured leaching consumables and chemicals for CIL operation. On the other hand, CNMC paid US$0.18mn pertaining to the proposed dual primary listing in Hong Kong. The total listing expense is expected to be no more than HK$5mn.

Outlook

In FY18, the primary catalyst that we look forward to is the significant turnaround of gold output, stemming from the replenishment of high-grade ore and higher gold recovery. Another positive factor is the resumption in the uptrend for gold prices. Meanwhile, we expect more capex from flotation facility construction and additional operating expenses from a planned dual primary listing in Hong Kong.

Source: Phillip Capital Research - 17 May 2018

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

RHB Investment Research Reports

2

Collin Seow Remisier Blog

3

THE SINGAPOREAN INVESTOR

Frasers Centrepoint Trust's Annual Report for FY2023/24 - Key Highlights to Take Note of

4

CEO Morning Brief

5

CEO Morning Brief

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....