Simons Trading Research

SingTel - Pressure All Over

Continued Outperformance Could be Challenging; Maintain HOLD

- SingTel's 1HFY19 core EPS was below consensus estimates at 43% of FY19E vs 51% for MKE.

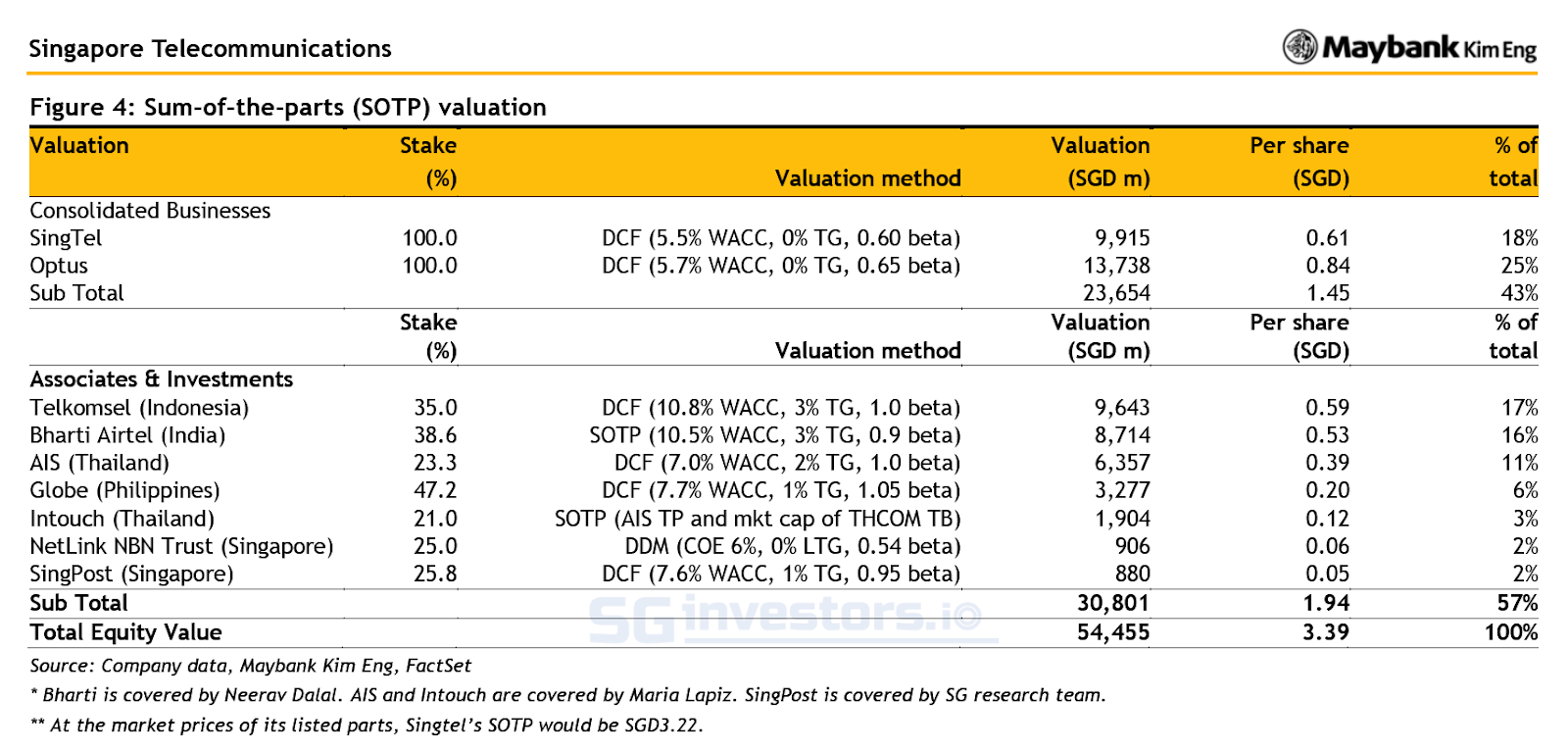

- We maintain our Singapore and Australia forecasts but reflect our house’s recent earnings revisions for Bharti and AIS. This lowers our DCF-based SOTP to SGD3.39 and our FY19E-20E core EPS by 4- 5%.

- Maintain HOLD as the stock’s continued outperformance could be challenging.

- Prefer its 25% associate, NetLink NBN Trust (SGX:CJLU), in Singapore’s telco space.

Consolidated Revenue in Line

- SingTel's 1HFY19 consolidated revenue met MKE/consensus estimates, at 48%/49% of FY19E.

- Heightened competition in the quarter was reflected in the increased popularity of SIM-only and data-add-on plans that diluted ARPUs. But thanks to Singapore’s healthy postpaid subs growth, non-escalation of hostilities in Australia and cost-management, we maintain our consolidated business forecasts.

Adjustments Made for Regional Associates

- We incorporate our colleagues’ latest associate forecasts for Bharti, whose results missed expectations. Although unlisted Telkomsel in Indonesia staged a q-o-q rebound from a partial recovery of data-pricing power, third-entrant risks have significantly increased for Globe in the Philippines.

- Overall, our SOTP and earnings are weighted more to Indonesia at 17% than the Philippines’ 6%.

Proverbial 20,000 Foot Tanker But All Seas Are Rough

- Singtel’s geographical diversification and non-wireless earnings base provide some protection against its Singapore wireless and broadband peers. This is reflected in its relative outperformance to the STI over the last one and three months.

- However, with competition in most of its markets outside Singapore in full swing or rising, we think absolute performance remains challenging.

Swing Factors

Upside

- Strong growth in enterprise and Digital Life to economies of scale.

- Ebbing competitive heat in India.

- Subsidies per smartphone drop.

Downside

- Wireless margin compression triggered either by TPG in Singapore and / or Australia or pre-emptive strikes by incumbents. These are not likely in consensus forecasts.

- Long-term capex for 5G rollout not likely priced in.

- Worse-than-expected cannibalisation of wireless voice, SMS and roaming by data.

Source: Maybank Kim Eng Research - 08 Nov 2018

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Simons Trading Research

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

Johor house best buy

HEXCAP (0035) TRANSGRID VENTURES VERSUS MN HOLDINGS: Compare & Contrast

2

STE's Stocks Investing Journey

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....