Simons Trading Research

CapitaLand - Replenishing Its China Land Bank

- Maintain BUY with a higher Target Price of SGD4.25, from SGD4.20, 36% upside and a 4% dividend yield.

- CapitaLand remains our Top large-cap Pick. This latest acquisition of a Chongqing site is a timely move to replenish its land bank. We believe the recent CapitaLand share price weakness stems from macro concerns on an escalation in global trade tensions which resulted in fund outflows from equities.

- Fundamentally, we expect sales and prices across its residential project in China to remain steady.

- We also expect it to benefit from a continuous build up in its recurring income base, with eight malls opening last year and a higher fee income.

Buying Chongqing Mixed-development Site for CNY5.7bn (SGD1.2bn)

The 32 hectare prime site is located in Xinpaifang, and is part of Chongqing’s Free Trade Zone.

The land parcel comprises of two greenfield sites that would yield 1,900 residential units and a shopping mall, as well as brownfield sites with an inventory of 223 residential units, along with office and retail space.

The project is expected to be completed by 2022.

China Residential Sales to Stay Resilient

In a recent report, our HK-based research team noted that with no new significant policy tightening, property sales in China and prices are expected to remain resilient in the near-term.

While there are concerns on the liquidity and rising funding costs, we believe this should not impact those developers with healthy balance sheets but instead it provides these with opportunities to do distress acquisitions.

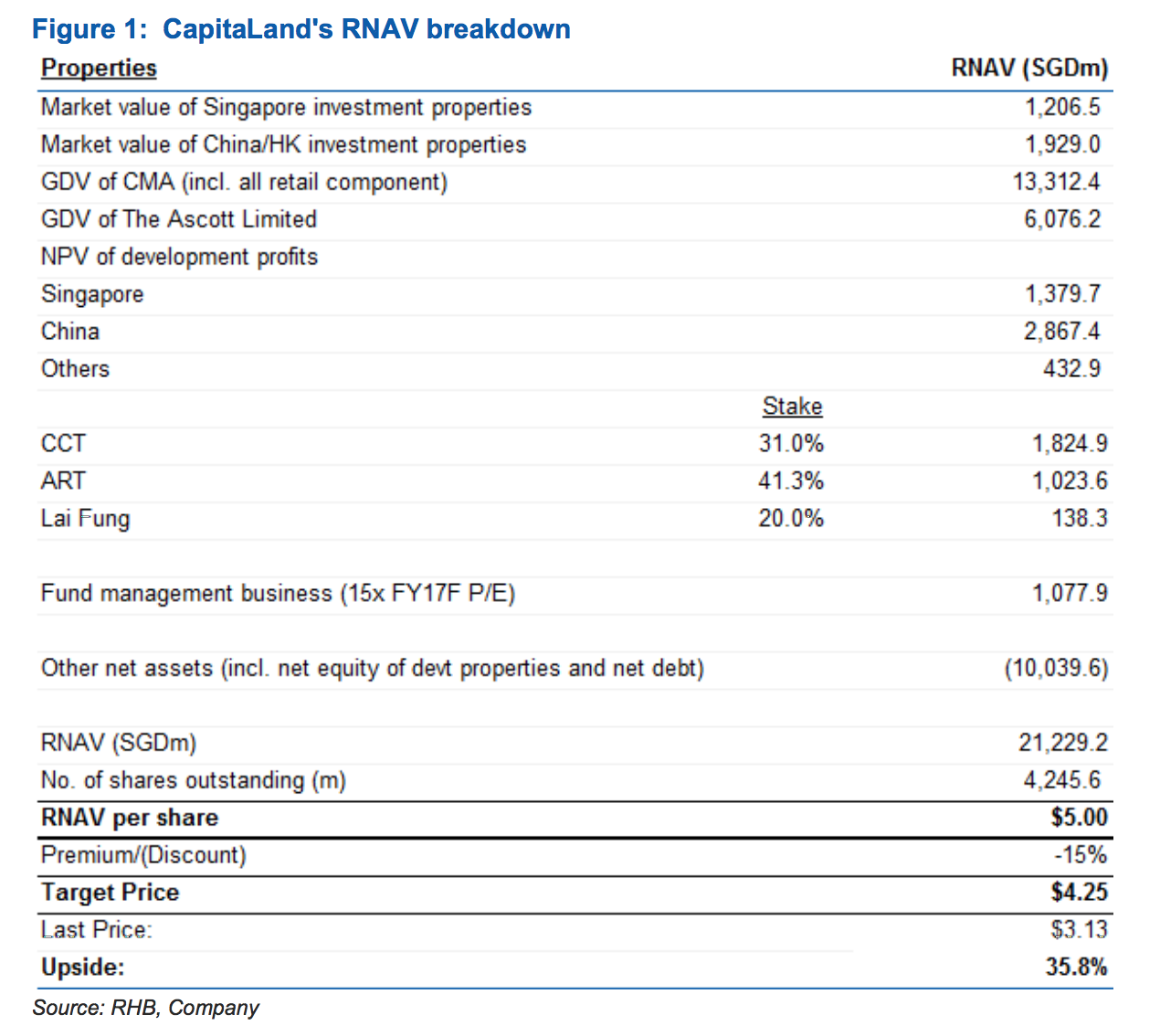

RNAV Accretion of 1%

We expect the total gross development value (GDV) for the site at CNY7.0-7.5bn. Management noted the ranges of residential prices around the area at CNY18,000-20,000psm and retail transactions at CNY25,000 – 28,000psm.

CapitaLand intends to do a strata sale of retail and also the office units over a period of time. Based on a blended average selling price assumption of CNY20,000psm, we expect a margin for the project at 20% with a 1% accretion to our RNAV.

A Timely Move to Replenish Its Land Bank in China

With the expected progressive handover of 8,000 units sold in China this year and the next, we see the move as a timely replenishment of its residential portfolio. The handover of units will result in a revenue recognition of CNY15.1bn, of which CNY10bn (or 70%) due to be recognised this year.

The acquisition would be funded by cash (39%) and the rest via local debt. Gearing is expected to increase marginally to 0.5x.

Our Top Large-cap Pick

Our Top large-cap Pick; BUY with a higher Target Price of SGD4.25, from SGD4.20, pegged at a 15% discount to our revised RNAV estimate of SGD5.00/share.

No changes to our earnings estimates as the overseas income can only be recognised upon completion, which we expect post 2020.

Source: RHB Invest Research - 28 Jun 2018

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Simons Trading Research

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Trade Confidently & Analyze Charts Conveniently - Download VCPlus IOS & Android App Now!

Latest Videos

Apps

Top Articles

1

SGX Market Updates

REIT Watch - S-REITs Navigate a Challenging 2024 With Mixed Returns

2

RHB Investment Research Reports

ComfortDelGro - Platform Fee Hike Is Earnings Neutral; Reiterate BUY

3

THE SINGAPOREAN INVESTOR

Frasers Centrepoint Trust's Annual Report for FY2023/24 - Key Highlights to Take Note of

4

CEO Morning Brief

Trader Who Made Billions in 2008 Returns to Bet on Market Swings

5

CEO Morning Brief

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....