A Path to Forever Financial Freedom

5 Financial Health Test That Determine Your Financial Robustness

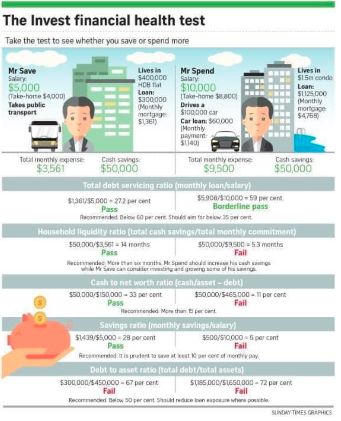

The Sunday Invest Section came out today with an interesting Financial Health Test to determine our financial health check conditions.

There are 5 sets of criteria that were used to test the financial robustness of a person's financial condition.

Let's go over them one by one.

1.) Total Debt Servicing Ratio (Monthly Loan Installment / Salary)

The debt servicing coverage ratio is a measurement of the cashflow available to pay current debt obligations for interest, principal and monthly installment payments.

This is a popular benchmark to measure the person's ability to produce enough cash to cover its ongoing debt payments.

For the majority of Singaporeans, most of the debt servicing is likely to come in the form of home mortgage, car and renovation loan. To ensure that Singaporeans are not over-leveraging, the TDSR ratio for property loans is set at a maximum of 60% while similar practice is being applied to other loans too. This is to ensure that most Singaporeans are not over-leveraging.

Verdict (for me): Pass

Comment: I feel like the ratio should extend just beyond salary because it is not the only income one might have. Nevertheless, using salary as a gauge seems conservative for now although I feel like the ratio should consider also the like of rental income, dividend and interest.

2.) Household Liquidity Ratio (Total Cash Savings / Total Monthly Commitment)

The household liquidity ratio is very similar to a corporation's current ratio, which measures the immediate needs for current assets over current liability.

For an individual, this will mean taking a person's cash availability over the total monthly expenses which includes not just the loan repayment obligation but also other spending categories such as grocery, transportation and utility charges.

The writer recommend that having 6 months worth of liquidity is a prudent gauge to have.

Verdict (for me): Fail

Comment: While I don't usually keep a lot of emergency cash lying around, my focus is catered towards accumulating more cashflow generating assets such as stocks, bonds and properties. For emergency requirement, I tend to rely on other immediate access tools such as credit cards or balance transfer account. This option is probably not as prudent enough as having 6 months worth of emergency requirement.

3.) Cash to Net Worth Ratio (Cash - Debt)

The cash to net worth ratio is very similar to the NCAV concept where you take in the good part of the assets (i.e cash) less all the liabilities that you owe.

Once again, you can see that the focus is very much on the amount of cash that you are holding so that alone stresses the importance of having sufficient cash in your overall portfolio allocation.

The writer recommends the ratio to be in excess of 15% to be considered good enough.

The writer recommends the ratio to be in excess of 15% to be considered good enough.

Verdict (for me): Fail

Comment: The same principle as above for me in terms of keeping cash requirement.

4.) Savings Ratio (Monthly Savings / Salary)

The savings ratio is a measurement of a person's savings rate from your salary.

In my opinion, this is the easiest requirement to meet because the writer recommended 10% as the minimum to save and I think most of us would have saved more than 10% of our take-home-pay.

Verdict (for me): Pass

Comment: It should measure take-home pay instead of gross salary because most Singaporeans will have automatic savings of minimally 37% through CPF (both employers and employees). The ratio should also be staggered increase over time to account for higher salaries or increase assets over time through inflation.

5.) Debt to Asset Ratio (Total Debt / Total Assets)

The debt to asset ratio is a measurement of the overall gearing allowance and a financial indicator of a person's financial leverage.

The writer recommends that this ratio should not exceed 50% and that he recommends reducing loan exposure where possible.

Verdict (for me): Pass

Comment: The ratio of 50% looks fair to me as you certainly don't want to be in a position where you over-leverage of things that doesn't generate enough returns for you. Still, with debt borrowings at an all time low these days, I can see a lot of people borrowing more debts to fund more generating assets in the years to come.

Conclusion

That's a score of 3 out of 5 for me.

Through this simple financial exercise, I can quickly see where my weak point is and that I should continue to work towards having more cash buffer as emergency as an overall part of my portfolio.

What about you? Did you check to see how your financial conditions are? Are there anyone who scored 5 out of the 5 based on recommended criteria?

Thanks for reading.

If you like our articles, you may follow our Facebook Page here

More articles on A Path to Forever Financial Freedom

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Trade Confidently & Analyze Charts Conveniently - Download VCPlus IOS & Android App Now!

Latest Videos

Apps

Top Articles

1

CEO Morning Brief

Singapore Post Shares Slide After CEO Fired Over Whistleblower Report

2

3

Johor house best buy

4

CEO Morning Brief

DBS Shares’ 43% Rally Seen Having More Legs as Wealth Fees Rise

5

CEO Morning Brief

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....