A Path to Forever Financial Freedom

10 Watchlist Target I Have During This Coronavirus Incident

In my previous article, I mentioned that I am likely to buy some of these companies in my watchlist from this week given their attractive entry point as they have dropped quite a bit since the start of the year or since the impact from the coronavirus event.

Here are my top 10 Watch list at the moment:

Here are my top 10 Watch list at the moment:

1.) Hongkong Land Holdings Limited (H78.SI)

I don't think Hongkong Land needs further introduction as it has been a theme play since the HK riot last year.

Hongkong Land is a property investment, management and development groups with premium commercial and residential property interests across Asia. It owns and manages almost 800,000 sq. m. of prime office and luxury retail property in key Asian cities, principally in Hong Kong and Singapore.

For years, many value investors and smart analysts have been trying to figure out why share price has been languishing way below NAV for a long while.

What is exactly the intrinsic value of HK Land and how it can bridge closer to the gap?

For one, we know that the NAV is USD16.50 and putting a conservative 40% discount to it we'll get USD9.90. If we want to go one step more conservative, we can further placed a 30% discount on the NAV revaluation since the HK riot is likely to impact the cap rate. If so, we'll get an intrinsic value of USD 6.93.

In my opinion, it is easier to play the range from the last 52 week low of USD 5.16 to USD 5.30 and sell it once it hits 10% upside (i.e in the range of USD 5.8) in the near term rather than waiting for value to converge to USD 6.93. The recent HK riot should be a good indication of where the market is pricing them in.

CFD Margin Requirement: 10%

Dividend Yield: 4%

Upside Potential (Minimally): 10%

Total Return Potential: 4% + 10% = 14% (with no leverage)

Total Return Potential: [(4% + 10%) x 2.5] - 3% = 32% (with 2.5x leverage)

2.) Greatview Aseptic Packaging Company Limited (0468.HK)

GA Pack's share price has been down close to 14% since the start of the year.

This is a company which my fellow friends in Value Invest Asia and Fifth Person's Dividend Machine has covered.

Greatview Aseptic Packaging offers an integrated packaging solutions, including provision of aseptic packaging materials and filling machines, mainly to the food and dairy industries across in China and International segment.

65% of the revenue comes from China and the dairy industry is struggling with demand, which probably signals why the share price has been impacted as of late. The International segment has been doing well and are exhibiting exponential growth, though it might take some time to pare against the China segment.

The company is likely to maintain their dividend payout at HKD 0.27/share, which translates to 8.7% yield at this price.

Dividend yield of 8.7% at a trailing PER of 7.2x, forward PER of 7.9x seems attractive enough for me.

The company also has a relatively strong balance sheet to grow their international segment further.

CFD Margin Requirement: None available

Dividend Yield: 8.7%

Upside Potential (Minimally): 10%

Total Return Potential: 8.7% + 10% = 18.7% (with no leverage)

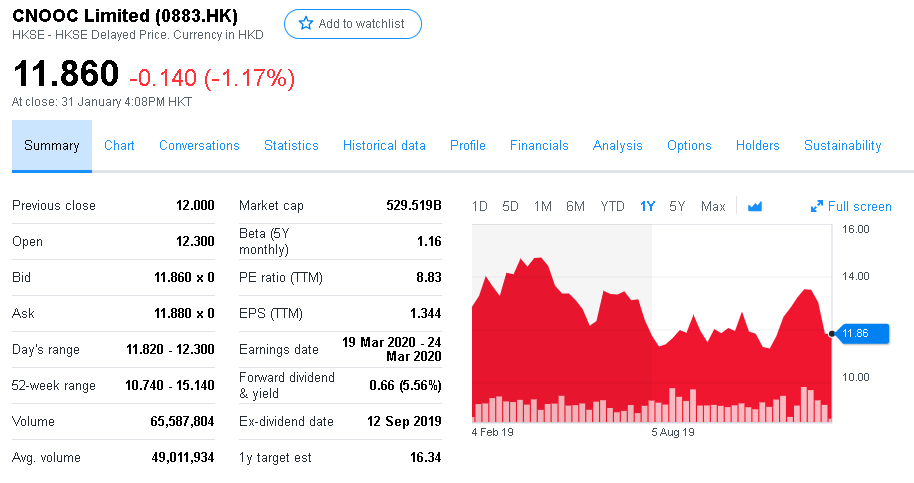

3.) CNOOC Limited (0883.HK)

CNOOC's share price has dropped about 8.5% since the start of the year mainly due to weak sentiment in oil prices and demand.

CNOOC is one of the largest national oil company in China.

What I like about the company is their ambition plans in the next 3 years strategy to increase production, pursue profitable reserves and continued exploration and production through increase in capex. Capex spent have increased from RMB 62.6bn in 2018 to RMB 80.2bn in 2019 and are expected to further increase to RMB 95bn in 2020.

Due to the strong cost structure and health margins, the company also generates plenty of operating and free cash flow that they have used to increase shareholders return, including increase the dividend payout over the years.

The 3 year rolling target is based on the project demand that has already been secured.

CNOOC is also a rolling theme macro play on demand for oil, so impact should be closely correlated to oil prices.

Dividend yield is at 5.9% and trailing PER of 8.8x, forward PER of 7.5X and 6.8x in the next 2 years.

CFD Margin Requirement: 10%

Dividend Yield: 5.9%

Upside Potential (Minimally): 10%

Total Return Potential: 5.9% + 10% = 15.9% (with no leverage)

Total Return Potential: [(5.9% + 10%) x 2.5] - 3% = 36.7% (with 2.5x leverage)

4.) Sinopec Shanghai Petrochemical Company Limited (0338.HK)

SSP's share price has been down 16.7% from the start of the year and is currently hovering near the 52 week low.

Sinopec Shanghai Petrochemical is one of the largest petrochemical enterprises in Mainland China. It has 5 distinct business units engaged in production of ethylene, synthetic fiber, resin and plastics, intermediate petrochemicals, petroleum products and commodities trading.

The company has been well on a battered run even prior to the Wuhan crisis since it announced its profit guidance that FY19 results was expected to decrease by RMB 2.8 to 3.2bn, representing a fall of about 55% year on year. Because of this, the company is expected to reduce dividend from the previous year of Rmb 0.25 / share to possible Rmb 0.20 / share, which still I think represent a good value at about 10% yield.

Management has provided guidance that refiner capacity production will continue to increase in FY2020 and assuming normalization of crude oil prices, could be key to maintaining the level of margins they had achieved in 2018.

Final earning results and dividend will be announced shortly so if we believe things are turning from here, investors could be buying the trough at this level.

5.) Wharf REIC (1997.HK)

Wharf REIC's share price has retreated close to 18% since the start of the Wuhan crisis and is hovering near the 52 week low.

8.) China Power International Development Limited (2380.HK)

China Power's share price has retreated by 10% since the start of the year, currently at the 52 week low and is hovering near the all time 2009 low of $1.39.

China Power International is a core subsidiary for conventional energy business of SPIC and operates businesses in coal-fired power, hydropower, nuclear power and renewable energy resources mainly across the mainland China.

9.) Tencent Holdings Limited (0700.HK)

Tencent's share price has dropped close to 8% since the start of the Wuhan coronavirus incident.

Tencent Holdings is a conglomerate and leader in multiple promising companies, including gaming, communications and advertising.

The advertising segment, which has been struggling for a while now, has seen some good improvement in the last quarter while gaming and communication segment has continued to perform well.

Current valuation at close to 40x PER does feel a little high to me at this point but as a growing leader with moat advantages this temporary one-off event may be a weakness to add.

10.) Wuxi Biologics (2269.HK)

Wuxi Biologics's share price has been resilient since the announcement of the Wuhan coronavirus incident.

WuXi Biologics is a Chinese headquartered organization that provides open-access, integrated technology platforms for biologics drug development.

Conclusion

These are some of the lists which I have been monitoring for a while, some of those are added recently due to the coronavirus incident while some have been in my watchlist for some time prior to the event.

Obviously, the lower the share price goes over the next couple of days or weeks, the more attractive the entry point is for me and I am likely to take a position in some of these 10 in my watchlist. When everything stabilizes, I think they have strong fundamentals to return to normalization.

P.S: No vested position yet as of writing but may take a position after writing.

SSP's share price has been down 16.7% from the start of the year and is currently hovering near the 52 week low.

Sinopec Shanghai Petrochemical is one of the largest petrochemical enterprises in Mainland China. It has 5 distinct business units engaged in production of ethylene, synthetic fiber, resin and plastics, intermediate petrochemicals, petroleum products and commodities trading.

The company has been well on a battered run even prior to the Wuhan crisis since it announced its profit guidance that FY19 results was expected to decrease by RMB 2.8 to 3.2bn, representing a fall of about 55% year on year. Because of this, the company is expected to reduce dividend from the previous year of Rmb 0.25 / share to possible Rmb 0.20 / share, which still I think represent a good value at about 10% yield.

Management has provided guidance that refiner capacity production will continue to increase in FY2020 and assuming normalization of crude oil prices, could be key to maintaining the level of margins they had achieved in 2018.

Final earning results and dividend will be announced shortly so if we believe things are turning from here, investors could be buying the trough at this level.

CFD Margin Requirement: 20%

Dividend Yield: 10%

Upside Potential (Minimally): 10%

Total Return Potential: 10% + 10% = 20.0% (with no leverage)

Total Return Potential: [(10% + 10%) x 1.5] - 3% = 27.0% (with 1.5x leverage)

5.) Wharf REIC (1997.HK)

Wharf REIC's share price has retreated close to 18% since the start of the Wuhan crisis and is hovering near the 52 week low.

Wharf REIC is a spin-off from the Wharf Holdings a couple of years back and has a business model of a typical REIT. Their main jewel properties include the Harbour City and Times Square, both of which are freehold in nature and are enjoying good traction of occupancy as well as lease retention.

Average current retail passing rent for Harbour City and Times Square are at HKD 508 / psf and HKD 290 / psf respectively. While HK retail sales are soft due to the riot and now the restriction of travel, lease rental outlook is stable and is expected to moderate at this level.

The company has a dividend policy of distributing 65% of the cashflow earnings and is expected to announce full year dividends at HKD 2.20 / share, which translates to 5.4% yield. At 100%, the company has a 8.3% strong earnings yield.

CFD Margin Requirement: 20%

Dividend Yield: 5.4%

Upside Potential (Minimally): 10%

Total Return Potential: 5.4% + 10% = 20.0% (with no leverage)

Total Return Potential: [(5.4% + 10%) x 1.5] - 3% = 20.1% (with 1.5x leverage)

6.) Bank of China (3988.HK)

BOC's share price has retreated by 10% since the start of the year and is hovering near a 6 months low.

Bank of China is a wholly state-owned commercial bank and has 11,752 outlets, of which 11,199 were in Mainland China.

BOC has one of the largest trade finance loan exposure among all the other big banks and is most vulnerable when there is uncertainties in the economy (e.g trade war, wuhan crisis, riot). NPL ratio has also risen in the last few quarters due to higher provisions though it started to get better in the 3rd Quarter when NPL ratio improved by 3 basis points.

The company currently has a dividend yield of around 6.8% and is trading at a P/BV of close to 0.5x, though further impairment is likely to impact the denominator.

In 2016 China crisis, BOC share price went as low as $2.91, so that is approximately the level I am looking to be adding.

CFD Margin Requirement: 10%

Dividend Yield: 6.8%

Upside Potential (Minimally): 10%

Total Return Potential: 6.8% + 10% = 16.8% (with no leverage)

Total Return Potential: [(6.8% + 10%) x 2.5] - 3% = 39.0% (with 2.5x leverage)

7.) Bank of Communications Co. Ltd (3328.HK)

Bank of Comm's share price has retreated by 12% since the start of the year and is hovering near the 52 week low.

Bank of Comm is the fifth largest bank in Mainland China and has in recent quarters one of the few that reported good set of results.

In the latest Q3 results, the company has posted quarterly net profit of Rmb 17.4m vs Rmb 16.5m the previous year. All other unit economics such as CAR, NIM and NPL has also improved to 12.7x, 1.57% and 1.47% respectively, showing healthy results on the back of a trade war uncertainties.

The company yields a dividend of 6.8% yield and is expected to announce its full year results shortly.

One thing to note however is if we take 2016 as a reference point, the company still has further room to fall especially if the China worsening escalates. Still, I think banks will be a beneficiary in this sort of Wuhan crisis as the government will allow less room for reserve ratio and thus should able to boost the loan growth.

CFD Margin Requirement: 20%

Dividend Yield: 6.8%

Upside Potential (Minimally): 10%

Total Return Potential: 6.8% + 10% = 16.8% (with no leverage)

Total Return Potential: [(6.8% + 10%) x 1.5] - 3% = 22.2% (with 1.5x leverage)

China Power's share price has retreated by 10% since the start of the year, currently at the 52 week low and is hovering near the all time 2009 low of $1.39.

China Power International is a core subsidiary for conventional energy business of SPIC and operates businesses in coal-fired power, hydropower, nuclear power and renewable energy resources mainly across the mainland China.

The company generates revenue through the sales of these electricity to different project pipelines.

In 2018, revenue increases by 16.1% to Rmb 23.1bn and this growth continued in 2019 as 1H revenue recorded a 27.9% increase year on year.

1H 2019 profits attributable to shareholders increased by 61.1% year on year.

The company has provided outlook for a favorable 2020 by increasing capacity for clean energy by 50% the current capacity.

Payout is near 100% with dividend yield at 8.3%.

CFD Margin Requirement: 20%

Dividend Yield: 8.3%

Upside Potential (Minimally): 10%

Total Return Potential: 8.3% + 10% = 18.3% (with no leverage)

Total Return Potential: [(8.3% + 10%) x 1.5] - 3% = 24.4% (with 1.5x leverage)

9.) Tencent Holdings Limited (0700.HK)

Tencent's share price has dropped close to 8% since the start of the Wuhan coronavirus incident.

Tencent Holdings is a conglomerate and leader in multiple promising companies, including gaming, communications and advertising.

The advertising segment, which has been struggling for a while now, has seen some good improvement in the last quarter while gaming and communication segment has continued to perform well.

Current valuation at close to 40x PER does feel a little high to me at this point but as a growing leader with moat advantages this temporary one-off event may be a weakness to add.

CFD Margin Requirement: 10%

Dividend Yield: 0.3%

Upside Potential (Minimally): 10%

Total Return Potential: 0.3% + 10% = 10.3% (with no leverage)

Total Return Potential: [(0.3% + 10%) x 2.5] - 3% = 22.7% (with 2.5x leverage)

10.) Wuxi Biologics (2269.HK)

Wuxi Biologics's share price has been resilient since the announcement of the Wuhan coronavirus incident.

WuXi Biologics is a Chinese headquartered organization that provides open-access, integrated technology platforms for biologics drug development.

A beneficiary in these sort of scenarios, the company said that they are exploring efforts to enabling the development of multiple neutralizing antibodies for 2019-nCOV with its integrated technology platform. The first batch trial is expected to be completed in 2 months, ready for preclinical toxicology studies and initial human clinical studies. Compared with the traditional timeline of between 12 to 18 months, Wuxi says they are able to complete their clinical antibodies by one-third the time given their extensive technology platform.

As a point of reference, the world first Zika virus antibody were completed in a record time of 7 months by Wuxi.

CFD Margin Requirement: None Available

Dividend Yield: 0%

Upside Potential (Minimally): 10%

Total Return Potential:10% (with no leverage)

Conclusion

These are some of the lists which I have been monitoring for a while, some of those are added recently due to the coronavirus incident while some have been in my watchlist for some time prior to the event.

Obviously, the lower the share price goes over the next couple of days or weeks, the more attractive the entry point is for me and I am likely to take a position in some of these 10 in my watchlist. When everything stabilizes, I think they have strong fundamentals to return to normalization.

P.S: No vested position yet as of writing but may take a position after writing.

Thanks for reading.

If you like our articles, you may follow our Facebook Page here

More articles on A Path to Forever Financial Freedom

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

THE SINGAPOREAN INVESTOR

Investing in Singapore's Hospitality Scene: A Look at the 5 Listed REITs

2

RHB Investment Research Reports

Food Empire - Expanding Ingredients Capability in Vietnam; BUY

3

RHB Investment Research Reports

ST Engineering - Rolling Forward Our Valuation; Reiterate BUY

4

CEO Morning Brief

Singapore Home Sales Set for Worst Year Since Financial Crisis

5

SGX Market Dialogues

Kopi-C With GuocoLand’s Group CEO: ‘We Have Twin Engines for Growth’

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....