A Path to Forever Financial Freedom

New Oriental Education - This Company Grows at 138% In The Past 12 Months

This is a company that has returned 138% in the last 12 months for investors as the company is looking to grow even more in the next few years which spells opportunities if you are looking into a growth play.

The company last closed at it's historical high at $122.72 and it is continuing to grow at a very fast double digit topline growth in the next few years.

Company Overview

Founded in 1993, New Oriental Education & Tech Group (NYSE: EDU) is the largest provider of private educational services in China. The company has an extensive network of over 1,261 learning centres that span across 56 different cities. New Oriental was the first successful Chinese educational institution to be listed in the New York Stock Exchange through their public offering back in 2016 and it has a market capitalization of over USD14 billion today.

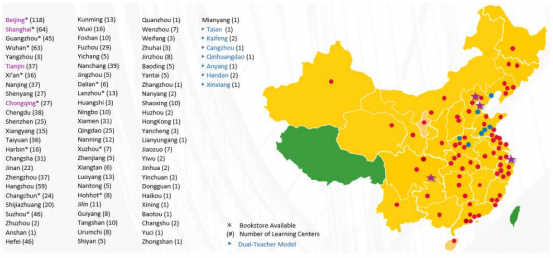

Growing Network: 1,261 and Counting

The company has a substantial presence in Beijing, Shanghai and Wuhan, where combined they have a total presence of 245 learning centres, or close to 20% of their entire portfolio.

Beijing: Beijing has one of the fastest growing population in China, as the number of people living in the city grew from 13.5m in 2000 to 20.1m in 2019 (source: worldpopulationreview). In terms of GDP per capita, Beijing has also outperformed the rest of the cities by growing at more than 8% per annum, despite the ongoing Trade Wars threatening the slowdown of their growing nation.

Shanghai: Shanghai currently ranks first in terms of population density as the modern revolutionized city appeals to International expats and locals to come to Shanghai for both work and live. It currently houses a population of about 26m but has the infrastructure capacity to double its living population in the city to 50m by 2050 (source: shine.cn) through their urbanization transformation in the region and strong economic growth.

Wuhan: Wuhan is a surprise inclusion because of its strong economic growth and infrastructure transformation over the years, the city has recorded one of the highest rate of historic population growth over the years (source: wiki-wuhan). To date, their population stands at about 10.6m, which is about half the population size of Beijing.

Financial Performance

Revenue has increased by 26.5% year on year from $2.4m in FY2018 to $3.1m in FY2019 and has grown at a CAGR of 19.8% over 5 years.

This is mainly due to both the organic aspect of growth (152 new facilities and learning centres added in FY2019) as well as inorganic growth through the successful implementation of the optimization strategy coming in from the K-12 After-School Tutoring division and U-Can Middle School, which grow by 28.5% and 27.2% respectively.

Gross Profit margins continued to remain resilient at 55.5% in FY2019, despite coming in slightly lower than the 5-year average of 57.3%.

As the company seek to embark on its expansion plan, the company has correspondingly incurred higher costs for marketing and other SG&A related costs such as salary and rent as there are higher headcounts to account for.

Operating and Net margins have dipped slightly to 9.7% and 7.7% in FY2019, which translates to a decrease of about 9.2% and 36% from the year before. The drop in net margins in FY2019 is mainly due to the revaluation loss of their long-term investments.

Cash-Flow Management

Cash Flow from Operations was approximately at $805m in FY2019, which is slightly higher due to better working capital and higher depreciation, as compared to $781m in FY2018.

Capital Expenditures came in at approximately $251m in FY2019 as the company continues its aggressive expansion plan by adding 152 new facilities and learning centres across the different cities.

The company's business model enables them to continue generating copious amount of Free Cash Flow, which stands at $553m in FY2019. This translates to an FCF yield of about 3.6% in FY2019, based on the last closing price at $96.58 (based on 31st May fiscal year).

Balance Sheet Strength

Due to the copious amount of Free Cash Flow that the company generates, the company is able to retain much of the retained earnings even after paying out dividends ($1.80/share) to shareholders.

As at 31st May 2019 (FY2019), the company has Cash Equivalent amounting to $1.41b and another $1.78 in Liquid Assets in their book. Net Cash stands at $3.1b, which is an increase of 14% over the previous year.

Net Cash & Cash Equivalent has grown at a CAGR of 20.86% over 5 years period.

From a valuation perspective, the company is not cheap but that's because the company is still growing at mid double digit topline growth, which signals there is plenty of rooms to grow both organically and inorganically.

From an earnings perspective, an EPS of 2 cents/share translates into an earnings multiple of 61x with the saturation growth continues to rampant through their ambition target.

FCF yield currently stands at 4% with growth capex incorporated into it as the company has very little maintenance capex to cater to.

The company also has plenty of room to maneuver their capacity utilization rate so optimization of capacity will be in play for any organic growth the company is utilizing.

With the amount of cash they continue to generate, it is likely the management can embark on both their expansion plan and returning more cash to shareholders.

Thanks for reading.

If you like our articles, you may follow our Facebook Page here

More articles on A Path to Forever Financial Freedom

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Trade Confidently & Analyze Charts Conveniently - Download VCPlus IOS & Android App Now!

Latest Videos

Apps

Top Articles

1

THE SINGAPOREAN INVESTOR

Investing in Singapore's Hospitality Scene: A Look at the 5 Listed REITs

2

RHB Investment Research Reports

Food Empire - Expanding Ingredients Capability in Vietnam; BUY

3

RHB Investment Research Reports

ST Engineering - Rolling Forward Our Valuation; Reiterate BUY

4

CEO Morning Brief

Singapore Home Sales Set for Worst Year Since Financial Crisis

5

SGX Market Dialogues

Kopi-C With GuocoLand’s Group CEO: ‘We Have Twin Engines for Growth’

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....