A Path to Forever Financial Freedom

Frasers Logistics Trust (FLT) Ventures Into Germany and Dutch Acquisitions

At around this time last year, FLT makes 7 Aussie assets acquisition and added them into their portfolio of the logistics predominantly located in parts of Australia.

This time round, they've gone a lot bigger by deciding to acquire 21 industrial properties, comprising of 17 properties in Germany and 4 properties in Netherlands which has a predominantly freehold land tenure.

The appraised value for these properties is valued at S$984.4m by independent valuers, and the agreed purchase price is at S$972.8m. This represents approximately 1.2% discount to the appraised value of the properties.

After deducting for the liabilities and debt facilities of the holding company, the purchase consideration after net is approximately around $515.4m. This is the amount that FLT has to come up with to acquire the 21 assets.

Assets Portfolio

The assets are spread across the different cities of Germany and Netherlands, with predominantly in Frankfurt, Stuttgart and Munich.

Majority of the land tenure are freehold in nature and this is common in what we see in Europe based on our understanding from Ireit and Hobee.

The properties are leased with 93% occupancy with an average WALE of 8 years. This increases the WALE of the portfolio from the current 6.4 years to 7.1 years based on post-acquisition.

I find the acquisition and properties solid because the Gross Initial and Net Yield for both the German and Netherlands properties are higher than the market prime yield in general.

This together with the NPI linked leases and long WALE I think bodes well for the acquisition.

DPU Accretive

The goal is to make the acquisitions accretive so both management and unitholders are happy with the situation.

I can see why some unitholders are sad that the yield accretive are only marginally higher in nature but this is what good management should be doing - to grow the AUM of the portfolio and at the same time marginally increasing the DPU while at the very same time protecting the balance sheet of the company.

If the company wants, they could have take this up through all the debts and we can have a higher DPU but it'll be bad for longer term.

Financial Modeling

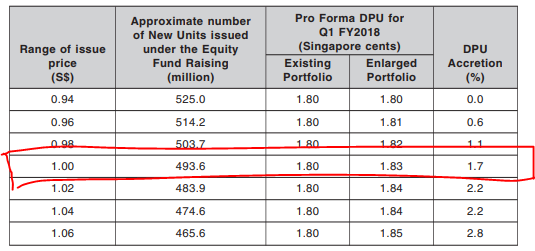

We know that the company has initiated an EGM on the 5th May to pass on the few proposed resolution before they can come up with the pricing on the preferential offering/rights issue.

The fact that they are only making this marginally yield accretive makes things easier for the management from the financial modeling point of view.

First, we know that the company needs to come up with S$515.4m worth of cash consideration for the purchase of the 21 properties net adjusted for liabilities, while the rest would be funded via inter-company loan agreement between the two SPVs.

Given FLT is trading at a premium to their NAV right now, it is more appropriate for the company to issue the financing via the equity since it also allows unitholders to participate in the growth.

The most likely scenario is a private rights issue for a 3 for 1 at a price for $1, which would yield the acquisitions slightly accretive. The good thing is we are far away from 94 cents so it is unlikely that they will issue that low which would make the yield destructive.

Final Thoughts

I think this is a good exposure to board FLT into a much bigger company with a lot bigger market cap after the acquisition.

Post-acquisition, the company will have 82 property assets that are held across Australia and Europe with a large portfolio value of $2.9B.

Statistics have shown that solid Reits who've done placement or rights at a premium to its NAV generally tends to do very well, so it'll only be a matter of time before we see the share price goes back to where they belong. If one cannot stand this minor noise we are undergoing, then I don't know how else you can get exposure to a good Reit.

I have a lot of exposures in this company, myself holding 100,000 shares and with the rest of my family members holding 35,000 shares on the rest, if this is a 3 for 1 at $1, then I am expecting to have a much larger position post the rights issue.

But this is something that I am definitely comfortable with holding.

Thanks for reading.

If you like our articles, you may follow our Facebook Page here.

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on A Path to Forever Financial Freedom

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

THE SINGAPOREAN INVESTOR

Investing in Singapore's Hospitality Scene: A Look at the 5 Listed REITs

2

RHB Investment Research Reports

Food Empire - Expanding Ingredients Capability in Vietnam; BUY

3

RHB Investment Research Reports

ST Engineering - Rolling Forward Our Valuation; Reiterate BUY

4

CEO Morning Brief

Singapore Home Sales Set for Worst Year Since Financial Crisis

5

SGX Market Dialogues

Kopi-C With GuocoLand’s Group CEO: ‘We Have Twin Engines for Growth’

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....