A Path to Forever Financial Freedom

Guest Post - Will QAF Rise Again?

Today, we have the honor of having Calvin from the InvestingNote to analyse for us the business of QAF Limited.

QAF is one of the stocks I personally used to own in the past but decided to let it go due to some business difficulties in Australia as far as I can remember

Brief background

QAF Limited (SGX: Q01) is a leading multi-industry food company with operations primarily in Singapore, Malaysia, the Philippines and Australia. It's core businesses include

1. Bakery

2. Primary production

3. Food manufacturing

4. Trading and logistics

5. Investments.

It owns household brands such as Gardenia and Bonjour under its bakery business segments and Cowhead and Farmland under its trading and logistics business segments.

Recent events and news

April 26, 'The Good And The Bad: What Investors Should Know About QAF Limited's Latest 2016 Results', refer to the news at: https://www.fool.sg/2017/04/06/the-good-and-the-bad-what-investors-should-know-about-qaf-limiteds-latest-2016-results/

April 5, QAF's annual report of financial year 2016, refer to the report at: http://www.qaf.com.sg/media/SGXAnnual%20Reports.pdf

April 1, 'QAF Limited Makes Money In 3 Different Ways: How Profitable Are They?', refer to the news at https://www.fool.sg/2017/01/13/qaf-limited-makes-money-in-3-different-ways-how-profitable-are-they/

February 24, 'QAF's FY2016 profit more than doubles to S$120.4m', refer to the news at http://www.businesstimes.com.sg/companies-markets/qafs-fy2016-profit-more-than-doubles-to-s1204m

January 10, 'QAF to invest S$21.5m to expand in the Philippines, refer to the news at http://www.businesstimes.com.sg/companies-markets/qaf-to-invest-s215m-to-expand-in-the-philippines

Performance summary

Overall, QAF has shown resilience in the financial year of 2016, amidst a challenging economic environment. ROE remains at a healthy 13% and PBT excluding exceptional items increased by 4%. Moreover, QAF maintained a healthy balance sheet and continued to pay steady dividends to its shareholders. It is interesting to note that QAF have plans to penetrate the halal food market by establishing new production plants in Malaysia that will export packaged bread to Islamic countries in Asia. Also, the factory currently undergoing construction in Malaysia will eventually replace the factory in Singapore when the latter lease expires and this will drive production costs down significantly. The stock price of QAF is currently on a downtrend.

Financial Highlights

QAF's revenue fell by 11% yoy, partially due to the deconsolidation of its Malaysia-based subsidiary, GBKL (Gardenia Bakeries (KL) Sdn Bhd), resulting in a fall in royalty fees collected. After adjusting for that one-off event, QAF saw top line growth with higher EBIT across all its business segments. Excluding the profits gained from the deconsolidation of GBKL, QAF's diluted EPS in 2016 would still have increased by 16% from 2015 and a substantial increase in net income margins from $5.3 million to $13.5 million.

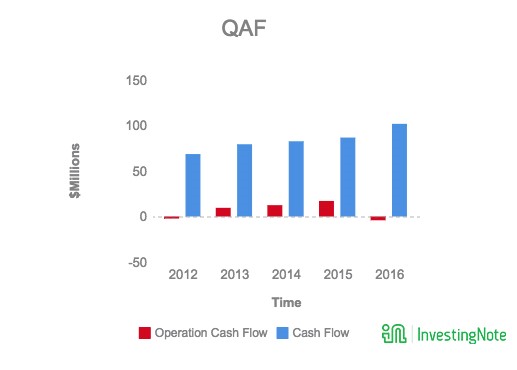

QAF reported a slight increase in assets despite the deconsolidation of GBKL as it entered into a joint venture for its Malaysian operations. QAF's net cash flows decreased to -$4.149 millon despite an increase in operating cash flows by $15.067 million due to a large decrease in financing cash flow to -$39.884 million. Correspondingly, they reported lower cash and cash equivalent in the balance sheet.

Traditionally, the bakery segment provides the lion share of the revenue. However, after the deconsolidation of GBKL, revenue from the primary production segment has overtaken the bakery segment for the first time in 2016. QAF's revenue was derived mainly from Australia, accounting for close to half of the total revenue, while its operations in Singapore and Philippines contributed similar but smaller amounts. Due to the deconsolidation of GBKL, the contributions from its Malaysia operations dropped sharply.

The underlying EPS of QAF is up 128% due to the deconsolidation of GBKL. QAF has a dividend yield of 3.82% at a P/E ratio of 6.121. Return on Equity (ROE) is 23.9% in 2016, a large increase from 12.4% in 2015, largely due to the deconsolidation of GBKL.

Peer comparison - QAF's biggest revenue contributors comes from its bakery and primary production business segment. Since QAF largest competitor in the bakery segment, Auric Pacific is undergoing privatization, thus I will choose two competitors from its primary production business segment. They are Japfa and ChinaKangdaFood.

Profit Margin - Across all the financial years since 2013, QAF has recorded higher profit margins than its competitors. From the chart, we can see that ChinaKangdaFood experienced negative profit margins in 2015, which is a potential red flag for investors. Also, Japfa experienced a dip in its profit margin in 2016, which may signal an erosion in their competitive advantage.

As shown in the chart, QAF has maintained its free cash flow from 2013 to 2016 as compared to Japfa, which recorded a sharp dive into negative free cash flow in 2016. Similarly, ChinaKangdaFood recorded negative free cash flow in 2015.

P/E ratio in 2016

QAF: 6.14

Japfa: 25.04

ChinaKangdaFood: 129.82

Food Industry: 23.688

Specialty Food Industry: 21.873

Data source: http://www.shareinvestor.com/fundamental/factsheet.html

In 2016, ChinaKangdaFood recorded the highest P/E ratio among the three companies. QAF is experiencing a downtrend in its P/E ratio while Japfa P/E ratio increased significantly year-on-year from 11.29 in 2015. Currently, QAF price has fallen from its high of $1.42 in February to $1.31. Similarly, Japfa is experiencing a downtrend in its price and is near its 52-week low. On the other hand, ChinaKangdaFood is experiencing a rally in its price ever since July 2016.

Key takeaways

In conclusion, QAF has developed strong economic moats as the market leader of the bakery segment in Singapore, Malaysia and Philippines in the past decades. Moreover, QAF controls Rivela, the largest fully integrated pork production company in Australia. Although the deconsolidation of GBKL resulted in a fall in revenue, this is expected to be temporary if its expansion into the halal food market succeed. QAF has proven itself to be a reliable defensive stock in today's volatile market. QAF is fully cognizant of the challenges such as an increase in competition and has come up with a 'strategy of sustainable growth and value creation'. All in all, if QAF manages to execute its strategy, it will continue to dominate its business segments and deliver sustained growth and dividends to shareholders.

Related estimates from other users

@llijiw, https://www.investingnote.com/posts/96951

@Spinning_Top, https://www.investingnote.com/posts/82373

@rubberducky, https://www.investingnote.com/posts/50868

For the original article, please refer to https://www.investingnote.com/posts/102752

This article is written by @calvinwee from InvestingNote.

Update (as of 5/5/17) - The company is undertaking strategic review on the proposed listing of the Primary Production Business in Australia or a sale of its business in its entirety.

More articles on A Path to Forever Financial Freedom

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

CEO Morning Brief

Singapore Post Shares Slide After CEO Fired Over Whistleblower Report

2

3

Johor house best buy

4

CEO Morning Brief

DBS Shares’ 43% Rally Seen Having More Legs as Wealth Fees Rise

5

CEO Morning Brief

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....