A Path to Forever Financial Freedom

Kimly Limited IPO - Should You Be Getting This?

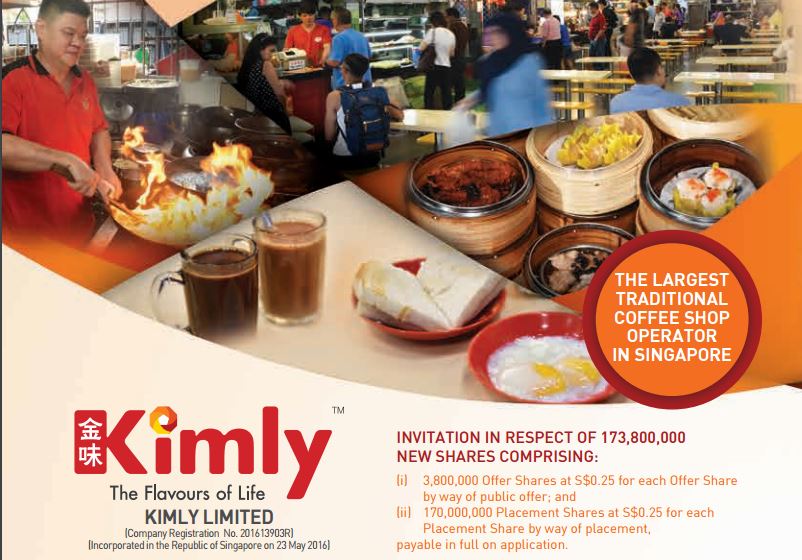

There's a new IPO in town and it's not any stranger to most neighborhood folks who have heard of the brand.

Kimly Limited is inviting man on the street to become part of the shareholders by opening a total of 173,800,000 new shares which comprises of 170,000,000 placement and 3,800,000 public tranche at an offer of $0.25 for each share.

|

| Indicative Timetable |

About The Company

Kimly Limited operates and manages coffee shops chains as the master leaseholder which then lease these food stalls to tenants.

They operates a total of 64 food outlets, which comprises of 56 coffee shops, 3 industrial canteens and 5 food courts.

They also had a central kitchen where all the activities for the food preparation was done at.

The current occupancy rate was at 98% and they own 5.8% market share of the business.

Financials

Let's first go to see the financials of the company.

The company had a decent cagr growth of 7.6% and 9.9% over the last 3 years. To be frank, this isn't hard to do when they have the cash to operate more food stalls to lease out given their impressive gross and net margins.

The company boasts an impressive gross margins of 21.5% and net margin of 14%. Do note however that profits attributable to shareholders are around 50/50 with the NCI.

We can see that the company operates under a light asset model.

Cash equivalent makes up around 67% of the total assets and that says all about it.

We can also see that cash turnaround trend is also great when they had such a remarkable less receivables and much higher payable on their books.

That says a lot about their business model.

In terms of Cashflow, they are also pretty much cash generative as they have such an impressive free cash flow generated.

Maintenance capex is low and is usually in the form of restoration costs and also some equipment changes.

Comparative Business Model

I've done some analysis on F&B companies in my past articles and draw up some pretty similar stats.

Kimly do not operate exactly under the same business model as Jumbo, Sakae, Tunglok and Japan food holdings but what we can see from the latter is that only Jumbo makes the cut outright successful in terms of the numbers. The other 3 has such a difficult time trying to reduce their overhead and increase productivity that their net margin remains low. The latter are also asset heavy which drags their roa and roi numbers downwards.

Perhaps it's better to operate under the Kimly model. It's asset light and cash generative. Though we are unsure if the options to grow are more limited that way.

Valuations

Valuation of the company is at 12x earnings and 5x book value.

I don't think it's the correct way to measure this via book value since they are asset light model so I would measure this via the free cash flow method.

If other F&B companies like Japan Food Holdings can be valued at 20x+ under such a heavy asset model, I think this might be valued higher.

12x earnings would look cheap if the company can grow well over the next 5 years.

My Thoughts

I do not quite understand the need for them to go public when they had so much cash in their book and they are generally cash generative.

I suspect the reason they go public is the need for branding as they are planning to open up an online ordering platform by partnering also with Ubereats and Grabeat.

When they do M&A, branding also plays an important part in tendering process.

With 3.8m shares on the public tranche, investors can expect to get nothing or little. Even if you are lucky, it'll be at most 3 to 5 lots.

I think this will debut well and will be valued much higher at around 18x earnings. I suspect share price would go to as high as 45 cents before settling down around there. With growth to come over the next few years, it might be well worth to see how well it can run from here, though of course execution risk is another matter altogether.

I'll try bidding this for fun and see how it goes. Maybe I can earn some free milk powder money in Mar :)

More articles on A Path to Forever Financial Freedom

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

CEO Morning Brief

Singapore Post Shares Slide After CEO Fired Over Whistleblower Report

2

3

Johor house best buy

4

CEO Morning Brief

DBS Shares’ 43% Rally Seen Having More Legs as Wealth Fees Rise

5

CEO Morning Brief

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....