The Boring Investor

Singapore Savings Bonds - A Year On

It has been a year since the launch of the first Singapore Savings Bonds (SSB) in Oct 2015. How have the interest rates of SSBs changed in this 1 year and how have they performed relative to the more conventional government bonds, namely, the Singapore Government Securities (SGS)?

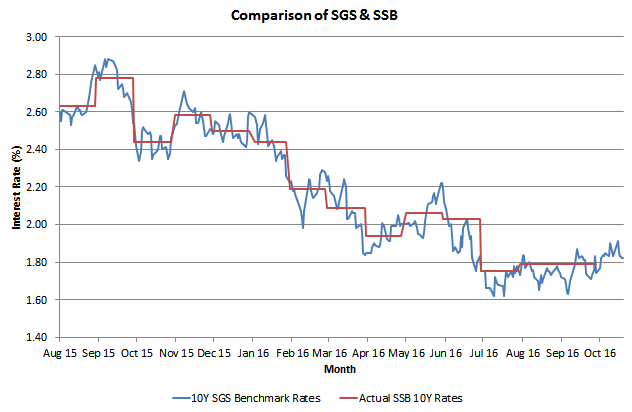

Fig. 1 below shows the 10-year interest rates of SSBs (red line). The interest rates are computed as the average of the benchmark 10-Year SGS interest rates (blue line) over the previous month. (Note: There is always a confusion over the "month" of the SSB. The SSB announced in Oct is issued in Nov and based on the average rates of the 10-Year SGS benchmark bond in Sep.). As you can see from Fig. 1, interest rates have been on a downward trend, reflecting the eagerness of central banks around the world to lower interest rates, to even negative levels in some countries.

|

| Fig. 1: SSB 10-Year Interest Rates |

The highest 10-year interest rate achieved for SSBs was for the second tranche of SSBs issued in Nov 2015. The interest rate was 2.78%. The 10-year interest rate touched a low of 1.75% for the tranche issued in Sep 2016. The interest rate for the current tranche is not much higher, at 1.79%.

If you had bought the first 2 tranches of SSBs issued in Oct and Nov 2015, you would be happy with your purchase, since interest rates for all subsequent tranches have been below these rates.

However, the performance of the more conventional 10-Year SGS bond was even better. Fig. 2 below shows the price performance of the 10-Year SGS bond since the issue of the first SSB.

|

| Fig. 2: Price Performance of 10-Year SGS and SSB |

On 1 Oct 2015, when the first tranche of SSB was issued, the 10-Year SGS benchmark bond traded at $98.61 for every $100 of bond principal. Due to the fall in interest rates, prices of bonds have been on the rise. A year later, on 30 Sep 2016, the same bond traded at $105.09. Investors who bought the SGS bond would have gained a capital appreciation of 6.6%. On top of that, investors would have received another 2.375% in coupons (i.e. interest) for holding the bond. Since investors bought the bond at less than the principal of $100, the coupons translate to an interest yield of 2.41% ($2.375 / $98.61). In contrast, SSBs are capital-guaranteed, which means that their value stays at $100 regardless of whether interest rates are going up or down. Over the same period, investors in the Oct 2015 SSB would have received 0.96% in interest, being the 1-year interest rate of the SSB. In total, investors in SSB and SGS would have received the following returns over the 1-year period.

| SSB | SGS | |

| Capital appreciation | - | 6.57% |

| Interest | 0.96% | 2.41% |

| Total | 0.96% | 8.98% |

Thus, the 10-Year SGS bond has outperformed the Oct 2015 SSB by as much as 8.02% over the 1-year period. The main reason is that interest rates have dropped from 2.54% in Oct 2015 to 1.74% in Sep 2016.

Hence, if interest rates are rising, it is better to stay with SSBs as they are capital-guaranteed. However, if interest rates are falling, SGS are a better choice as they will gain in price. By juggling between SSB and SGS, you can gain from changes in interest rates. This is exactly the conclusion discussed a year ago in Getting the Best of Both SSB & SGS.

See related blog posts:

More articles on The Boring Investor

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Trade Confidently & Analyze Charts Conveniently - Download VCPlus IOS & Android App Now!

Latest Videos

Apps

Top Articles

1

RHB Investment Research Reports

United Overseas Bank - 2025 Shaping Up to be An Interesting Year

2

RHB Investment Research Reports

OCBC Bank - More Patience Needed on Capital Management Plans

3

SGX Market Updates

SIA Engineering Resumes Buybacks After Reporting H1 FY2025 Results

4

RHB Investment Research Reports

Venture Corp - Soft Demand Delaying 2H Recovery; Maintain BUY

5

CEO Morning Brief

Singapore Airlines Vows to Expand Capacity Despite Rising Competition

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....