The Boring Investor

Understanding the Accounting for Joint Ventures

Perennial has successfully launched its second, 4-year, 4.55% retail bond this week. For a discussion on whether the bond has sufficient margin of safety, you can refer to the analysis for its first retail bond here. The purpose of this post is to discuss the accounting treatment of joint ventures (JVs) and associates, using Perennial as an example as it has a fairly detailed breakdown of them.

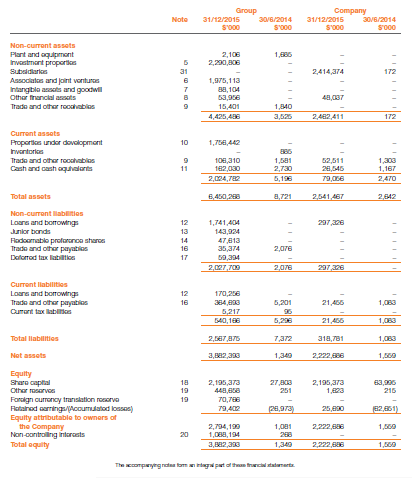

Fig. 1 below shows Perennial's balance sheet as at Dec 2015, extracted from its annual report. As the info in the screenshots are rather small, please refer to the annual report for better clarity of the info.

|

| Fig. 1: Perennial's Balance Sheet |

As shown in the figure above, it has total current and non-current loans, borrowings and bonds of $2,055.6 million (shown in lines 12 & 13 in Fig. 1). Note that there is an item called "Associates and Joint Ventures" in the non-current assets that amounts to $1,975.1 million (line 6). Associates and JVs are generally consolidated in the balance sheet on a net asset basis. For example, assuming there is a 50-50 JV which has assets of $100 million and liabilities of $20 million, its net asset is $80 million. On the parent company's balance sheet, this JV will show up as an asset of 50% of $80 million, or $40 million. Its 50% share of the $20 million liabilities will not show up in the balance sheet. Likewise, neither will its 50% share of the $100 million assets show up in the balance sheet. The equity of the parent company is unaffected whichever way associates and JVs are accounted for.

Is it important to bring back the assets and liabilities of associates and JVs to the parent company's balance sheet? Yes, because it provides a clearer, look-through picture of the amount of debt that the parent company is carrying. For JVs, the rationale is quite clear, because the parent company has some control over the JV, similar to a subsidiary. For associates, however, it is quite subjective as the parent company may or may not have any control over it, depending on its shareholding in the associate.

Let us use Perennial as an example to understand how to bring back the borrowings of JVs and associates to the parent company's balance sheet. On page 218 of Perennial's annual report, there is a fairly comprehensive breakdown of the company's investments in JVs and associates and their respective assets and liabilities, as shown in the figures below.

|

| Fig. 2: Perennial's Investments in JVs and Associates |

Fig. 2 above provides an overview of Perennial's investments in JVs and associates. Besides equity investments, Perennial also makes shareholder loans to JVs and associates. Thus, when we discuss Perennial's share of borrowings in the JVs and associates later, we need to deduct its shareholder loans to avoid double-counting.

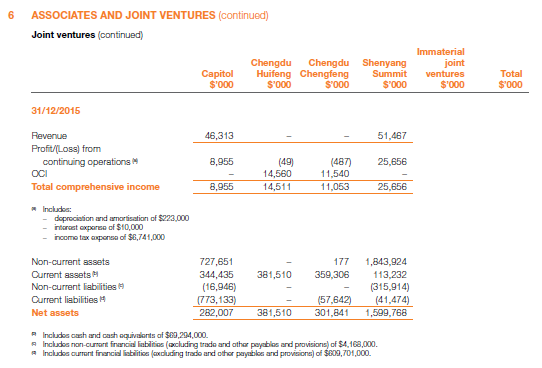

|

| Fig. 3: Breakdown of JVs' Assets and Liabilities |

Fig. 3 above shows that Perennial has 4 material JVs which have total current and non-current liabilities of $1,205.1 million. Not all of them are borrowings. In the footnote to the footnote, it states that the current and non-current financial liabilities are $609.7 million and $4.2 million respectively. Deducting Perennial's shareholder loans of $71.1 million, the net financial liabilities are $542.8 million. Perennial's shareholding in all these 4 JVs is 50%. Hence, Perennial's share of the JVs' borrowings is $271.4 million.

|

| Fig. 4: Breakdown of Associates' Assets and Liabilities |

Fig. 4 above shows Perennial has 3 material associates, with shareholding ranging from 30% to 46.6%. There is no further footnote to indicate the amount of borrowings in these associates. In such cases, a reasonable assumption is to assume that non-current liabilities are mostly borrowings while current liabilities are mostly accounts payable. Perennial's own balance sheet in Fig. 1 shows this to be the case, where borrowings make up 93% of the non-current liabilites and 32% of the current liabilities. Using this assumption, the associates' borrowings are estimated to be $822.1 million. Deducting Perennial's shareholder loan of $74.8 million, the net associates' borrowings is $747.2 million. After accounting for Perennial's shareholding in the associates, its share of associates' borrowings is $233.1 million. If we apply the same assumption to the JVs' borrowings, Perennial's share of JVs' borrowings would be $130.9 million instead of the $271.4 million mentioned above.

We are now ready to bring back Perennial's share of borrowings in JVs and associates to its balance sheet. Perennial's borrowings shown in the balance sheet are $2,055.6 million as mentioned earlier. Its share of JVs' borrowings is either $130.9 million (based on non-current liabilities) or $271.4 million (based on footnote disclosure). Assuming that we want to be conservative and account for its share of associates' borrowings, another $233.1 million needs to be added. Thus, on a conservative basis, Perennial's look-through borrowings are between $2,419.6 million and $2,560.1 million. The look-through borrowings are $364 million to $504.5 million more than that shown in the balance sheet.

In conclusion, the usual accounting practice for JVs and associates is to show them as a single line item in the balance sheet on a net asset basis. The proportional share of assets and borrowings of JVs and associates do not show up. To have a clearer, look-through picture of the parent company's borrowings, it is necessary to look into the footnotes and adjust for the company's share of JVs' and associates' borrowings.

More articles on The Boring Investor

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

CEO Morning Brief

Singapore Post Shares Slide After CEO Fired Over Whistleblower Report

2

3

Johor house best buy

4

CEO Morning Brief

DBS Shares’ 43% Rally Seen Having More Legs as Wealth Fees Rise

5

CEO Morning Brief

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....