Trader Hub

Singapore Airlines – Declining Yields

traderhub8

Publish date: Thu, 09 Nov 2023, 11:36 AM

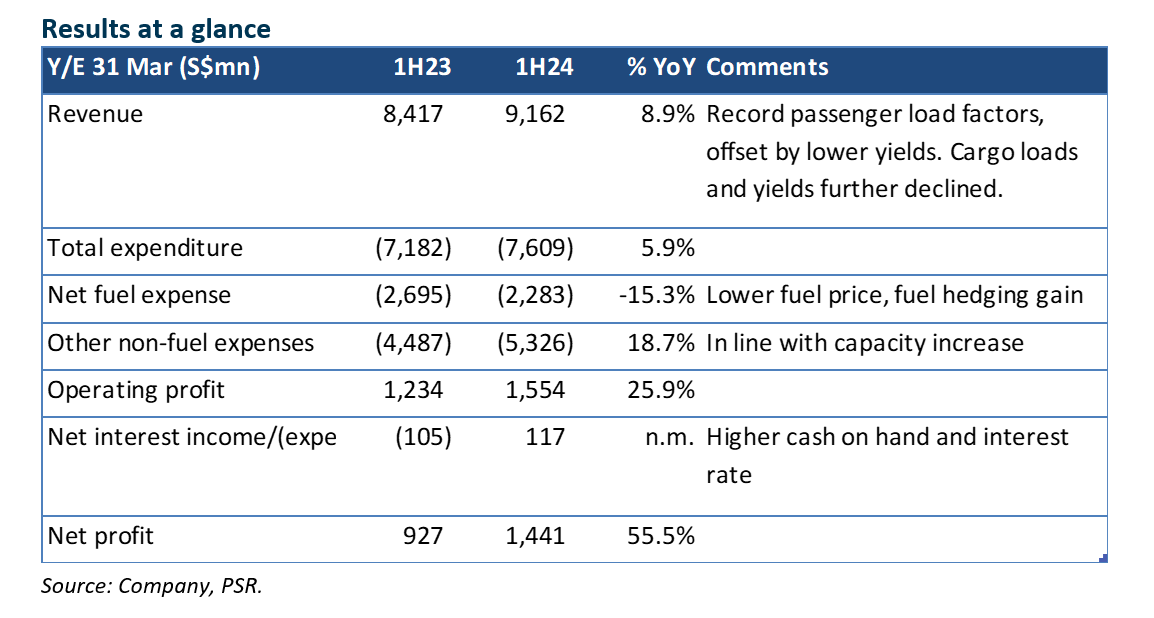

- 1H24 net earnings beat our estimates, at 82% of our FY24e forecast. It surprised us with an 18.8% YoY lower fuel bill despite the higher capacity and a S$244mn gain from fuel hedging. We raised our FY24e estimates by 14.3% to factor in the stronger 1H earnings.

- Growth was driven by strong passenger load (+38% YoY), while yields have begun to fall (-8.5%). Cargo remains weak as volume (-6.0%) and yields (-46.2%) were lower, though yields are above pre-Covid levels.

- SIA plans to redeem 50% of the remaining Mandatory Convertible Bonds (MCB) for S$1.71bn, bringing total redemption to S$5.1bn for FY24e.

- We maintain a REDUCE recommendation, and lower our TP to S$5.45 (prev. S$6.80), at 1x FY24e P/B (prev. 1.1x). This takes into account an ex-growth operating environment with yields and loads under pressure from increased competition and the fading off of travel demand.

The Positives

+ Higher passenger load offset decline in yields. Robust demand mainly from leisure travellers lifted passenger loads by 38.0% YoY. This helps to offset the decline in passenger yield such that revenue per available seat-km (RASK) only fell 2.0% YoY to 9.6 cents.

+ Lower average jet fuel price and fuel hedging gain. Average jet fuel price before hedging achieved was 29.2% lower YoY at US$105/barrel, and it booked a hedging gain of S$244mn (1H23: S$417mn). We had expected its jet fuel price to rise in 2Q in line with the market.

+ Higher net interest income. It booked net interest income of S$117mn from higher interest rate from net cash of S$5.2bn at end Mar 23.

The Negative

– Cargo remains a weak spot. In line with weaker trade flows globally and bigger capacity added from the return of passenger flights, cargo yield fell 46.2% to 41.8 cents/load tonne-km. This is however, still higher than pre-Covid of about 31 cents.

Outlook

Heightened competition from restoring capacity mainly from the North Asian airlines and a fading off of leisure travel will put pressure on yields. Jet fuel price is trending higher along with higher crude oil prices. We expect capex spending to rise in 2H to meet its target of S$2.3bn for FY24e (1H24: S$648mn). It would also incur cash outlay of S$5.1bn in FY24e for the redemption of MCBs and S$600mn for convertible loan. This would lower interest income in 2H.

Maintain REDUCE and lower TP to S$5.45, from S$6.80 previously, which is based on 1x FY24e book value (prev. 1.1x). We have raised our FY24e net profit estimates by 14.3% to factor in the strong 1H.

Source: Phillip Capital Research - 9 Nov 2023

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

Singapore REITs Monthly: April24 – Pricing in Higher-for-longer Interest Rates

Created by traderhub8 | May 20, 2024

SASSEUR REIT – FY24e Sales Will be Driven by Promotional Events

Created by traderhub8 | May 15, 2024

ST Engineering Ltd – All Engines Roaring, But Satellite No Signal

Created by traderhub8 | May 14, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Apps

Top Articles

1

2

CEO Morning Brief

Singapore Air Staff Get Eight Months' Salary Bonus After Record Profits

3

CEO Morning Brief

Singapore's First New PM in 20 Years Holds Inaugural Cabinet Meeting

4

Trader Hub

5

RHB Investment Research Reports

ComfortDelGro - Seasonally Weak 1Q24; Better 2H24 Expected; BUY

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....